Markel is a diversified financial holding company that operates in three distinct segments: Insurance (60% of 2023 revenue), Investments (5%), and the Company’s private equity division, Markel Ventures (35%). In 2023, Markel generated a total of $14.3 billion in revenue and $1.6 billion in adjusted operating income (11.1% margin), and on December 31, 2023, book value per share was $1,096. The Markel share price has suffered temporary drawdowns following its past two quarterly results, as insurance underwriting profitability has been underwhelming. Long-term shareholders are frustrated by continued underwriting losses in the reinsurance segment, the lack of any recent acquisitions in Markel Ventures, and several self-inflicted wounds from management, including challenges at the Markel CatCo insurance-linked securities operations.

Unlike many public corporations, Markel‘s management team has exhibited honesty and integrity regarding these challenges—a testament to the organization‘s culture. Despite these missteps, book value per share has continued to compound at an attractive double-digit rate: 17% in 2023 and an 11% compound annual growth rate over five years. We estimate that Markel‘s intrinsic value has compounded even faster. This is due to the increasing contribution from Markel Ventures, where book value is a less relevant metric—the amortization of intangible assets depletes book value. At the same time, unrealized losses on the company‘s bond portfolio, a large portion of which is likely to reverse over the coming thirty months.

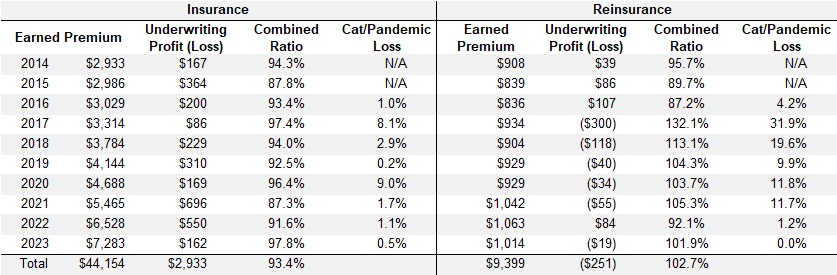

Markel‘s insurance operations delivered poor underwriting results in the second half of 2023. The most important contributor to this higher-than-anticipated combined ratio was a greater reserve build for projected losses in the North American casualty and professional liability product lines—particularly the company‘s construction business due to unexpectedly higher inflation since the onset of the pandemic. With a new management team for its insurance business, Markel is positioned to put this adverse loss experience behind it and expects a better combined ratio in 2024. We believe this is likely, particularly given the idiosyncratic losses in 2023 and the substantial restructuring of the reinsurance portfolio. While 2023 saw challenges in the reinsurance line and portions of the casualty and professional liability lines, large parts of Markel‘s insurance operations performed exceptionally well, including the property, marine and energy, small commercial, personal, and surety product lines and the Markel International segment—each of which delivered double-digit premium growth and outstanding profitability.

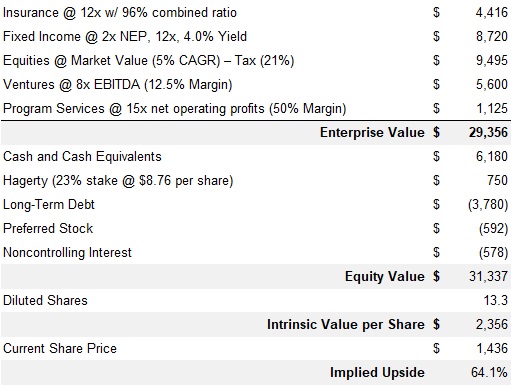

Using a sum-of-the-parts valuation framework, we obtain an intrinsic value estimate of $2,356 per MKL share based on 2026 estimates, representing an upside of ~55% from current levels. Our valuation equates to a price-to-book multiple of approximately 1.6x—a value that Markel shares traded at or above for 2016-2019 and that they regained in late 2022/early 2023, which appears conservative for a company that consistently generates double-digit book value per share growth. Insiders seem to agree that shares are currently overly discounted, judging from the acceleration in share repurchases and purchases by eight directors over the past two years. As an alternative indication of undervaluation, we note that Markel shares trade at ~13x 2023 adjusted net profit—a valuation multiple almost half the current 25.3x P/E multiple of the S&P 500 without accounting for the company‘s net cash balance sheet and while employing a conservative estimate for capital gains on the equity portfolio.

Markel Corporation is a diversified financial holding company that operates in three distinct segments.

Insurance (60% of 2023 revenue) comprises the company‘s insurance and reinsurance underwriting operations, fronting platforms, and insurance-linked securities (ILS) investment operations. In 2023, this segment delivered $8.3 billion and a combined ratio of 98.4% for the underwriting divisions, alongside revenue of $263 million (50.8% margin) from the fronting and ILS operations.

Investments (5% of 2023 revenue) produced $717 million in 2023 from investment income net of investment and other expenses. This segment includes the investment of premiums paid by insurance policyholders into high-quality government, municipal, and corporate bonds that generally match the duration and currency of expected claims. As of December 31, 2023, the portfolio had an average rating of AAA and an average duration of 4.1 years.

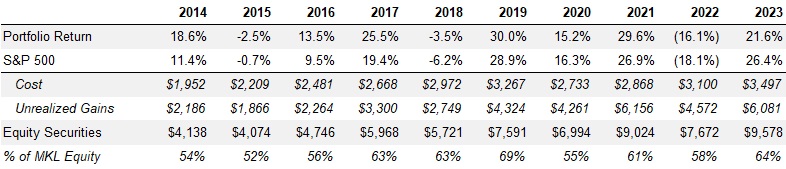

Markel also invests underwriting and other company profits into equity securities. The equity portfolio has averaged 60% of shareholder equity over the past ten years, respectively. Nearly all the portfolio is managed by company employees, and the equity investments are intended to be held over the long term, with an unrealized gain of $6.1 billion as of December 31, 2023.

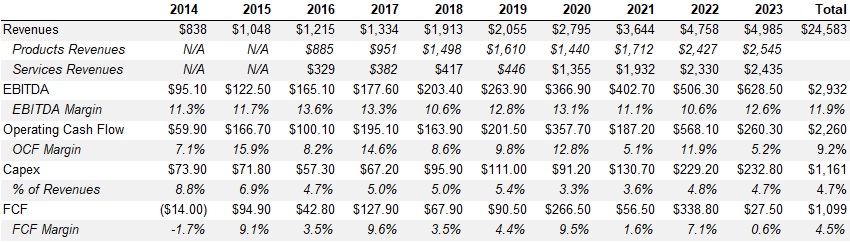

Markel Ventures (35% of 2023 revenue) involves wholly owned subsidiaries or controlling interests in specialized industrial businesses. In 2023, this segment delivered $4.99 billion in revenue with a profit margin of 12.6%. Products (51% of segment revenue) include consumer and building-related products (ornamental plants, residential homes, luxury handbags), transportation-related products (car haulers, tube and tank trailers, truck flooring), and equipment manufacturing products (commercial baking equipment, dredges). Services (49% of segment revenue) include construction services (building products distribution, crane rental, and fire protection), consulting services (technology and retail data analytics), and healthcare, leasing, and investment services.

The company’s restructured insurance portfolio is set for improved performance. In 2023, Markel delivered poor insurance underwriting results. The most significant contributor to this higher-than-anticipated combined ratio was a greater reserve build for projected losses in the North American casualty and professional liability product lines—specifically contractor excess and umbrella and primary general liability casualty (concentrated in the construction business) as well as the risk managed errors and omissions (E&O) and directors and officers (D&O) product lines in professional liability.

This reserve build is predominantly the result of higher inflation since the onset of the pandemic, not only economic but also social inflation: the propensity for juries to award more frequent and punitive litigation settlements for a range of reasons, such as changing societal attitudes, increased attorney representation, increasingly aggressive plaintiff bar tactics and more frequent involvement of third-party litigation financiers. A report by Marathon Strategies showed that the sum of corporate “nuclear verdicts” (>$10 million) increased from $6 billion in 2015 to over $18 billion in 2022.

As higher loss trends emerged, Markel increased its loss reserves in 2022 and 2023. Still, the deterioration in 2023 prompted a more thorough review of the insurance portfolio, leading to increased provisions. The review, which involved a much deeper assessment of the causes of adverse developments, was conducted at a very granular level and enlisted third-party experts to assess broader industry trends for comparability. In addition to the increased provisions, the review resulted in several changes to improve the management of the insurance portfolio: exiting unprofitable classes and subsegments, reducing areas of excessive concentrations, adjusting terms and conditions, limits, attachment points, and pricing, and making various personnel changes. CEO Gayner expects an improved combined ratio in 2024. We think this is likely, particularly given the idiosyncratic losses in 2023 associated with credit losses, bank failures, and the company‘s now discontinued intellectual property collateral protection insurance and as we move beyond the weaker insurance pricing from years before 2020.

However, reinsurance challenges continue to overshadow the insurance segment’s profitability. Underwriting losses in Markel‘s reinsurance segment have been a recurring theme since it acquired Alterra in 2013. In the past ten years, this segment has produced cumulative underwriting losses of approximately $251 million, including losses in six of the past seven years. By contrast, the insurance division has generated a cumulative underwriting profit of $2.9 billion. Markel‘s insurance operations were significantly restructured in 2020, with reduced exposure to natural catastrophes and property reinsurance no longer underwritten from 2021. Notably, catastrophe losses within the reinsurance segment have been materially reduced. Unfortunately, due to the already discussed inflationary trends, Markel created additional provisions within its casualty lines to account for these emerging loss trends, particularly in its general liability writings and public entity lines. This business has since been discontinued.

But, there are several reasons to be optimistic, with 2023 seen as a blip in the turnaround of Markel‘s reinsurance segment and future profitability expected to improve again. Markel has refreshed the leadership team, catastrophe losses appear to have been mitigated following the property restructure, the underperforming public entity business has ceased, additional provisions are now in place for policies written before the hard market, and we are now moving into a company that was written with adequate pricing. Although CEO Gayner supports the Reinsurance business and is attracted to its operating leverage, he may be open to exiting the business if results do not improve in the next several years. European holding company Exor sold its reinsurer PartnerRe in 2022 to French mutual insurer Covea for $9.3 billion, representing a 29% premium to book value. While this represented an attractive sale price relative to global peers, selling Markel‘s reinsurance business at a premium to book would be highly accretive and positive if underwriting results do not improve.

While 2023 saw challenges in the reinsurance and portions of the casualty and professional liability lines, large parts of Markel‘s insurance operations performed exceptionally well. The property, marine and energy, small commercial, personal, and surety product lines, representing more than a quarter of premiums, had outstanding results. These well-established businesses have attractive growth prospects and are expected to continue producing solid underwriting results. The performance of Markel International was also excellent, similarly delivering double-digit top lines and profitability. Markel has expanded into Australia and parts of Europe in recent years, and management sees further opportunities for expansion in the years ahead.

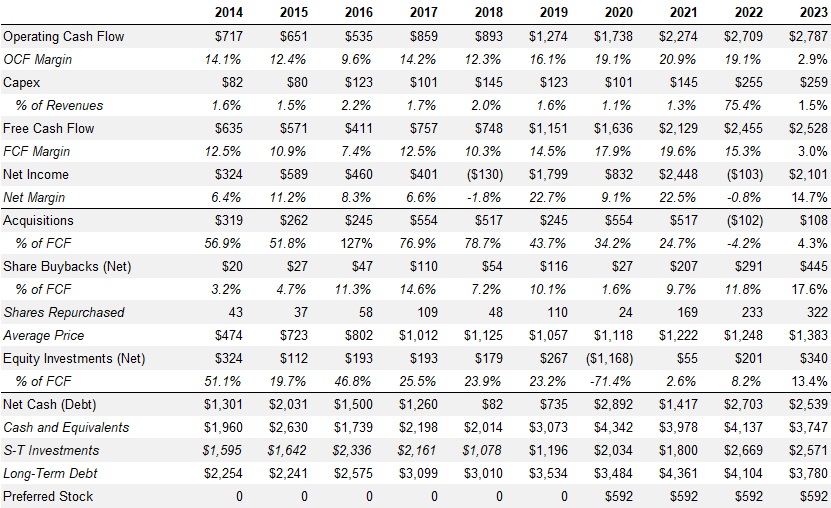

Markel Ventures continues to post impressive financial results. The higher revenues reflected increased demand, higher prices, and growth at the construction services and transportation businesses and increased production at an equipment manufacturing business, partly offset by lower demand at the consumer, building products, and consulting services businesses, along with one construction service business. Operating profit margins increased to 24.1% while profit margins averaged 12.6. Wall Street remains somewhat circumspect regarding Ventures, given Markel‘s historical insurance-focused investor base, the relatively low reported margins for the segment, and the reasonably limited financial disclosure that Markel provides for the individual Ventures subsidiaries. However, return on capital is a function of both margin and inventory turns. Mr. Gayner noted that the company‘s distribution businesses may be low-margin but generate excellent returns on invested capital.

Further supporting Markel Ventures‘ financial strength, Mr. Gayner disclosed in the 2023 letter to shareholders that since its inception in 2005, Ventures has delivered $1.7 billion in dividends to Markel Group, compared with a purchase price total of $3.7 billion. Notably, this $3.7 billion includes only $1.4 billion in equity contributions from the parent company, with the remainder funded by intercompany loans and ongoing cash generation from the existing Ventures businesses. This is a helpful guidepost that suggests a high return on equity. We model our estimates of Ventures‘ free cash flow, which support the strength of its cash flow capabilities with more than $1 billion in cumulative free cash flow over the past ten years—including solid growth in specific years when growth from the insurance operations was more limited, supporting its diversification merits.

More than two years have passed since Markel completed its last large-scale Markel Ventures acquisition, a 51% stake in precast concrete manufacturer Metromont, in December 2021. Mr. Gayner has remained disciplined in his valuation framework, and the sustained period of low-interest rates since the global financial crisis and outsized growth in private equity has significantly increased competition for the middle-market companies that Markel typically targets. However, the steep rise in benchmark interest rates is beginning to create an environment more conducive to acquisitions, dampening private equity activity and placing some smaller companies under increasing financial stress, mainly labor and supply chain pressures. While it will take some time for private market valuations to adjust fully, Mr. Gayner has indicated that inbound call activity has been at the highest level in the past eighteen months, and he is increasingly confident that a period of sustained higher interest rates will lead to greater deal activity. In support of this thesis, Markel was able to execute two small bolt-on deals early in 2024 at fire safety service provider VSC and indoor plant producer Costa. The Company remains well-positioned to finance any potential opportunity at short notice, with a net cash position of approximately $2.5 billion as of December 31, 2023. We believe this would be sufficient to finance a deal of up to $1 billion.

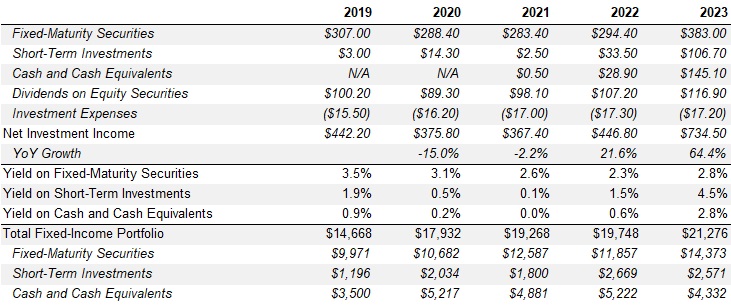

Markel‘s net investment income increased 64.4% to approximately $735 million in 2023. Excluding dividends on equity securities included in this consolidated number and increased 9.0% year-over-year, investment income from the fixed-income portfolio increased 81.9%! This growth was fueled by an increase in the size of the fixed-maturity securities portfolio and increased yields on the back of higher benchmark interest rates. Despite this massive step-up in 2023, substantial further upside remains for Markel‘s investment income should benchmark interest rates remain close to the prevailing levels. Additional disclosure in the 2023 annual report indicates that the yield on Markel‘s $14.4 billion bond portfolio yielded only 2.8% in 2023—far below the prevailing yield curve, which averages 5%.

Markel operates a plain vanilla fixed-income portfolio that invests in insurance reserves that match the estimated claim duration. While this has severely depressed the company‘s investment income over the past several years, it also provides the opportunity for continued uplift as maturing fixed-income securities are progressively reinvested at higher yields. Based on an average portfolio duration of 4.1 years as of December 31, 2023, we estimate that the yield on Markel‘s fixed-maturity securities portfolio could increase ten basis points per quarter over the coming two years, delivering an extra $115 million in annual pretax income by the end of 2025. Coupled with the anticipated growth in the size of the fixed-income portfolio based on further insurance premium growth, we see a combination that should deliver materially higher net investment income. This is likely to be achieved with minimal investment risk, based on a portfolio containing high-quality government, municipal, and corporate bonds, with 97% of the portfolio rated AA or better.

Markel‘s equity portfolio has not received much attention recently. Still, it has remained a strong performer despite the challenges of 2020 and a more value-focused tilt to the portfolio amid a stock market that has rewarded growth companies lately. These results have been achieved with minimal turnover, creating a tax-efficient compounding structure for shareholders. In fact, with a cost base of only $3.5 billion as of December 31, 2023, Markel‘s unrealized gains approached $6.1 billion at year-end, for a total portfolio value of $9.6 billion, representing 64% of shareholder equity and over 30% of the current market capitalization. Markel‘s investment strategy is also exceptionally cost-efficient, with investment expenses of only $17.3 million in 2023, roughly flat over the past three years and representing 0.2% of the equity portfolio, or just 0.06% when combined with the company’s fixed-income assets.

Markel generates exceptional free cash flow due to the nature of the insurance business with its low capital requirements, negative working capital cycle, and the strong cash generation of the Markel Ventures business. The Markel Group‘s capital expenditures have averaged only 1.7% of revenues over the past ten years, with free cash flow exceeding net income by 49% over the same periods. This discrepancy results from a growing insurance business, the size of the equity portfolio, and the amortization of intangible assets. This is despite the increasing importance of the Markel Ventures business. Despite relatively modest insurance premium growth, Markel generated an extremely strong $2.5 billion in free cash flow last year, 3% higher than in 2022 and equating to a free cash flow yield of 13%.

Mr. Gayner‘s priorities for capital allocation state: (1) reinvestment in organic opportunities within the insurance or Ventures businesses, (2) acquisitions of additional Markel Ventures or insurance companies, (3) purchase of public equity securities, and (4) repurchase of Markel stock. Within this framework, every incremental dollar is invested with the thought of where it will generate the highest return. The strength of Markel‘s ability to generate free cash flow allows it to pursue these reinvestment alternatives while maintaining an excellent balance sheet with minimal leverage. Markel has maintained a net cash position in the past ten years, providing the company with a margin of safety and the ability to rapidly close on any potential opportunities, which can often be prompted by sudden intergenerational transfer or liquidity concerns.

Substantial free cash flow generation and the absence of any platform acquisitions in 2023 enabled Markel to deploy a net $340 million into equity securities, adhering to Markel‘s long-standing four-part investment test: (1) profitable companies with good returns on capital, (2) run by honest and talented management, (3) with reinvestment opportunities and capital discipline, (4) available at a fair or reasonable price. Additionally, Markel considerably accelerated its share buyback program, repurchasing $445 million in stock in 2023—roughly 322,000 shares at an average price of $1,383 per share. Share buybacks have now totaled $943 million over the past three years, proving that management believes the intrinsic value of Markel shares far exceeds the current trading price.

Estimate of Intrinsic Value

Markel‘s underperformance has been stark on a medium-term basis, with a return of 53% over the past five years, compared with a 99% total return for the S&P 500. This is mainly due to multiple compression, with the price-to-book multiple decreasing from 1.6x five years ago to 1.4x today. During 2018 and 2019, the company’s multiple was even higher at 1.8x-1.9x. Notably, this is despite book value per share growth of 17.1% in 2023 and a five-year compound annual growth rate of 10.8%. Additionally, this growth rate was achieved despite a drag of $459 million ($35 per share) in accumulated other comprehensive loss (AOCI) associated with the fixed-income securities portfolio (as of December 31, 2023), the majority of which should accrete back to shareholders over the coming two to three years, and the depletion of nearly $828 million in intangible asset amortization ($63 per share).

As Warren Buffett put it in Berkshire Hathaway‘s 2016 letter to shareholders, recording charges against other intangibles, such as customer relationships, arises from purchase-accounting rules and does not reflect economic reality. By contrast, goodwill and intangible asset impairments are more likely to represent an actual loss of monetary value to shareholders, and one should not adjust these out. Adjusting for AOCI and intangible asset amortization, we estimate that book value per share increased at an annual rate of 12.8% over the past five years.

Given the differences between the Insurance and Ventures businesses and the size of the equity portfolio, we value Markel shares using a sum-of-the-parts framework. We incorporate underwriting operations using an estimated net earned premium of $9.2 billion, a combined ratio of 96%, and a pretax multiple of 12x, implying a price-to-earnings multiple of fifteen based on a tax rate of 21%. We view the fixed-income portfolio as part of the insurance operations and value it based on an income stream rather than an asset value. Using the leverage of twice the net earned premium, an estimated portfolio yield of 4.0%, and a pretax income multiple of 12x (15x P/E), consistent with the insurance operations. For Markel Ventures, we assume revenue growth of 4%, net operating profit margins of 12.5%, and a multiple of 8.0x (a discount to reflect the lack of transparency).

Our valuation equates to a price-to-book multiple of approximately 1.6x—a value that Markel shares traded at or above before 2019, which appears conservative for a company that consistently generates double-digit growth in book value per share. Insiders seemingly agree that shares are currently overly discounted, judging from the acceleration in share repurchases and purchases by management and directors.

Additionally, despite current trends, we have incorporated no accretive capital deployment, such as share repurchases below our estimate of intrinsic value or Markel Ventures acquisitions, both of which appear likely in 2024 and beyond. Finally, if insurance underwriting results improve, this would materially affect our valuation, with each 1% of the combined ratio equating to $90 per share of additional intrinsic value.

As a company with significant property and casualty insurance underwriting operations, Markel may experience losses from man-made or natural catastrophes. Markel seeks to manage its loss exposures in various ways, including adhering to maximum limitations on policies written in defined geographical zones, implementing maximum gross limits by coverage for each insured, establishing per-risk and occurrence limitations for each event, employing coverage restrictions, and following prudent underwriting guidelines for each program written.

Significant periods often elapse between the occurrence of an insured or reinsured loss, the reporting of the loss to Markel, and its payment. To recognize liabilities for unpaid losses, Markel establishes reserves as balance sheet liabilities representing estimates of amounts needed to pay reported and unreported losses and the related loss adjustment expenses. Estimating loss reserves is a challenging and complex exercise involving analytical models with many variables and subjective judgments. This process has also become more difficult in the current period of rising inflation.

Other company risks include, but are not limited to, capital allocation, particularly sizable insurance or Ventures acquisitions; the loss of key personnel, particularly CEO Tom Gayner; macroeconomic conditions, particularly inflation (CPI and social) and deep recessions, insurance competition, and cyclicality within the industry. There is also risk associated with Markel Ventures‘ geographic concentration in Virginia.