“You can’t predict. You can prepare.” -Howard Marks.

Meteorologist Edward Lorenz is best known for the “butterfly effect,” the idea that a slight disturbance, like the flapping of a butterfly’s wings, can provoke enormous consequences. As told in the book “Chaos,” in 1961, Dr. Lorenz ran weather simulations using a simple computer model.[1] He wanted to repeat one of the simulations. Instead of repeating the entire simulation, he started the second simulation in the middle, typing in numbers from the first batch run for the initial conditions. Because the computer program was the same, the weather patterns of the second simulation should have matched the first results. Instead, the two weather trajectories diverged on entirely separate paths.

Initially, Dr. Lorenz suspected a computer malfunction. But upon closer inspection, he realized he had not entered the same initial conditions. The computer stored the numbers with a precision of six decimal places, but the printout truncated the numbers to three decimal places for space-saving purposes. When Dr. Lorenz re-entered the numbers, he used the three decimal numbers. This minor discrepancy led to a complete alteration in the results. Dr. Lorenz realized that weather prediction was a mere illusion. A perfect forecast would necessitate an ideal model and flawless knowledge of wind, temperature, humidity, and other conditions worldwide at a single moment in time.

Dr. Lorenz was not the first to discover chaos theory. At the end of the nineteenth century, the mathematician Henri Poincaré showed that the gravitational interaction of as few as three bodies was hopelessly complex to calculate, even though the underlying equations of motion seemed simple. Poincaré considered one of the originators of the mathematics underlying chaos theory, worked on what is known as the “three-body problem.” In short, a three-body problem refers to a system solvable not through an elegant algorithm but only through brute-force computation. There is no closed-form solution to predict the future locations of three planetary bodies in a vacuum, like the Earth, the sun, and the moon. Edward Lorenz and Henri Poincaré reached their conclusions in a deterministic physical world. In contrast, economic and financial forecasts deal with a far more complex environment—human emotions.

Sentiment is an unpredictable variable that can drive market outcomes. Financial markets exist to price the risk of capital efficiently and accurately. Rusty Guinn of Epsilon Theory observed that financial markets mostly behave like two-body systems.[2] The interaction of Planet A (fundamental data) and Planet B (prices) is generally predictable. While information takes time to propagate, market participants also know that Planet C exists, far enough away that its gravity induces only short- and medium-term distortions in the relationship between fundamentals and prices. If one knew Planet A and B’s starting positions and velocities, one could determine where prices should be within a margin of error, but that is often not the case.

Once upon a time, a better investor meant using traditional security analysis to uncover the truth about Planet A and predict Planet B’s future location (price). Yet even the devoted Graham and Dodd fundamental disciple recognizes markets where Planet C’s gravity influences the system in hard-to-understand ways. Among those periods where one’s ability to invest based on fundamentals relative to securities prices is especially poor is during bubbles and manias. Sir John Templeton, an influential twentieth-century American-born investor, noted, “The four most expensive words in the English language are ‘This time it’s different.’” It is never different, but something has changed in today’s markets. Artificial intelligence and cryptocurrencies cannot explain current valuations. One suspects that financial markets may no longer serve as a mechanism for price discovery. Markets have morphed into a political utility, a tool to protect the wealth and stability of our political structures. Once meant to stabilize business cycles, monetary policies now act as tools to prop up financial asset prices while central bankers employ communication narratives to support political policies. Planet C’s gravity now dominates markets.

One wonders how the utility of public security markets morphed into such a state. Murray Stahl, chairman of investment firm Horizon Kinetics, provided his timeline of events that influence today’s markets.[3] Since 1980, Murray remarks that most investors have only experienced a disinflationary environment. The historical narrative credits the U.S. Federal Reserve Bank under Paul Volcker’s leadership in raising interest rates to an appropriately high level, slowing the economy enough that pricing pressures relented. Murray argues that the world of 1982, particularly the industrialized world as it then existed, benefited from a series of economic miracles that had nothing to do with the U.S. Federal Reserve.

With the Soviet Union on the verge of financial collapse during the 1980s, the country used its only source of external hard currency: commodities. The Soviets possessed every hard commodity, from oil and coal to diamonds; all they could do was sell them on the global market. When the Soviet Union ultimately collapsed, so did its economic circumstances. The country desperately needed cash, resulting in more pressure on the selling price of their commodities. After the Cold War, this previously unavailable supply flooded the market and broke the back of commodity price inflation.

Murray then cites the People’s Republic of China as the next massive disinflationary force to shape the global economy. Although China desperately needed cash and could not offer commodities, it had a population of one billion. Rather than sell commodities, China offered the world its enormous low-cost labor pool. Like China, eventually Vietnam, Thailand, the Philippines, India, Pakistan, Indonesia, and Malaysia offered their low-cost labor pool. Labor in the industrialized world lost their power to negotiate for higher wages.

In addition to the disinflationary impact of commodities and labor, after 1990, major consumer brand companies that could once only expand globally within the “free world” could now be truly global. Global expansion ensued, with growth that would not otherwise have occurred. Where it was once impossible for McDonald’s to open a store in Bucharest or Warsaw, now they could. Murray’s three economic tailwinds created enormous economic change. Diminishing inflationary pressures permitted central banks to reduce interest rates. Lower interest rates encouraged financial engineering. Financial assets eventually replaced tangible assets as the preferred form of holding wealth.

One tailwind that Murray neglected to mention is the enormous economic benefit of the shale revolution in the United States. The United States is unique because the landowner owns the hydrocarbon resources underneath their property, unlike elsewhere in the world, where governments own subsurface mineral rights. With access to investment capital, abundant industry expertise, and the rule of law, the United States is a leading oil and gas producer. Few appreciate the importance of shale oil production growth, the only source of non-OPEC production growth over the past two decades. Between 2010 and 2020, U.S. shale oil and natural gas liquids production grew by 11.6 million barrels per day, more than Saudi Arabia’s production of 10.5 million barrels per day. Shale gas production grew an incredible 65 billion cubic feet per day over the same period. When converted to barrels of oil equivalent, U.S. shale gas added another 10.8 million barrels per day, comparable to a second Saudi Arabia.[4]

In just ten years, U.S. oil companies brought online double the equivalent of Saudi Arabia’s output, an incredible achievement in a world that depends on hydrocarbons to sustain a modern life and support continued economic productivity. Powered by low commodity prices, an enormous new labor pool, genuinely global markets, and the shale revolution, financial markets have enjoyed a period of generationally low interest rates. With decades of ever-lower interest rates, governments’ interest expense burden declined, providing governments with more money to spend.

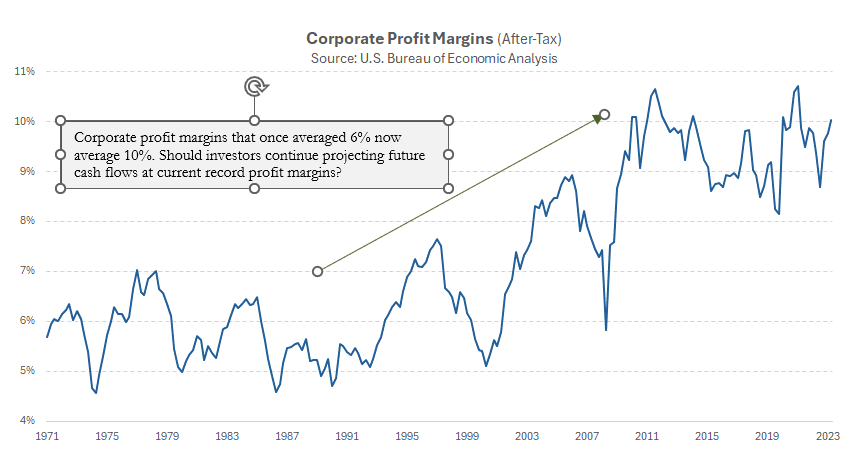

This additive government spending padded economic growth. Corporations benefitted from these tailwinds that resulted in extraordinary global expansion, cost-of-goods-sold profit margin benefits, labor cost benefits, debt and equity funding cost benefits, and fiscal expansion benefits. Do these tailwinds continue, or have financial markets already enjoyed their benefits? Markets appear convinced that current record profit margins are the correct basis for projecting future cash flows for decades to come.

For value investors, the S&P 500 has been nearly impossible to outperform over the past decade and, most certainly, the last year. The U.S. equity market has grown more concentrated, with the largest stocks outperforming. To outperform an index, logically, an investor must differ from the index. This difference distills down to the stocks an investor owns and what stocks he decides not to own. Typically, a value investor holds a bias against the largest stocks in their benchmark index, particularly investors who favor a concentrated portfolio. For most of history, biasing portfolios against the largest stocks has been rewarding, but it has been a disaster over the last decade, particularly last year.

Since 1957, the ten largest stocks in the S&P 500 index have underperformed an equal-weighted index of the remaining 490 stocks by 2.4% per year. The last decade notably deviated from that trend, with the largest ten stocks outperforming by a massive 4.9% per year on average. The continued, unrelenting outperformance of the largest companies has led to the S&P 500 becoming significantly more concentrated over the past decade. The top seven names in the index comprise 28%, up from 13% a decade earlier. Ten years ago, the index was more than twice as diversified. According to investment firm GMO, over any ten-year period, the market has never experienced a decline in diversification of the magnitude just experienced.[5]

If less diversified, the market is undoubtedly more efficient in creating bubbles. They appear faster than ever but narrower in scope. The most recent mini-bubble centers around the obsession with artificial intelligence (AI), with a handful of stocks soaring. Opinions differ in definition, but a bubble is when an asset no longer moves on fundamental information. The asset price increases as new buyers enter the market because “price go up.” George Soros, a legendary hedge fund manager, observed this behavior in his theory of reflexivity. Financial asset prices are one of the few things where demand can increase as the price rises. A rising stock price should theoretically make the asset less attractive. Nonetheless, human nature sees the rise in price as confirmation that they are correct, reinforcing their buying propensity. This reflexive behavior lies at the heart of all bubbles.

Markets are too unpredictable and complex to predict with any measurable confidence level. Financial price reflexivity adds to the confusion as markets grow increasingly institutionalized with the dominance of passive investment vehicles. With State Street’s introduction of the first exchange-traded fund (S&P 500 Trust ETF or SPDR) in 1993, the slight disturbance of the “butterfly effect” induced enormous future investment consequences. Price analysis dominates today’s decisions on financial assets held by passive vehicles. Quantitative analysis is replacing fundamental analysis. A quantitative approach emphasizes and exploits the movement of liquidity among asset classes. With more money being managed quantitatively, there is an increase in momentum-chasing strategies. New ideas are quickly recognized and then morph into reflexive price-chasing mini-bubbles. The difficulty is when market participants can no longer differentiate whether the asset is a good investment for fundamental reasons and if it is going up because others are chasing price momentum.

With the world awash in too much cash, Wall Street eagerly develops new products and structures to accommodate that cash. The byproduct is less volatility as prices steadily rise but lower future returns. Periods of high returns like 2023 and the first quarter of 2024 will intermittently appear, but that heavily depends on the liquidity support governments provide. On a fundamental basis, businesses can generate only so much profit in a global economy drowning in debt. Today’s extreme stock valuations are aided and abetted by the market structure and monetary policy factors. Market structures in the form of ETFs and other passive investment products direct money to the biggest stocks like NVIDIA Corporation (NVDA) without investors understanding what they are buying.

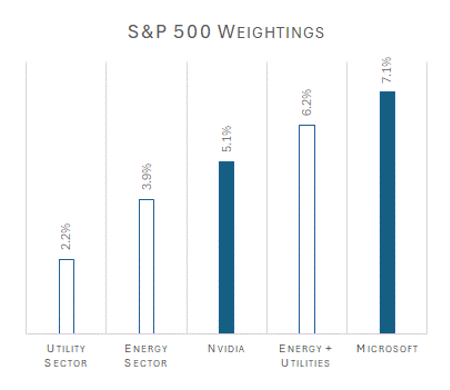

As the AI frenzy grips Wall Street, Nvidia sits at the epicenter, with a current market value of $2.3 trillion. To put this hype into perspective, Nvidia constitutes 5.1% of the S&P 500 Index, while the energy sector accounts for only 3.9%. Meanwhile, the top ten energy companies generated annual revenue eighteen times greater than Nvidia’s trailing sales and four times greater net income.[6] Of course, AI supporters might argue there is no measurable upside limit to the future potential of artificial intelligence usage or implementation throughout the world economy. The contrarian might say there is better value in the energy companies unless Americans no longer wish to enjoy the comforts of modern life.

“Vast swaths of the United States are at risk of running short of power as electricity-hungry data centers and clean-technology factories proliferate around the country, leaving utilities and regulators grasping for credible plans to expand the nation’s creaking power grid,” read a recent headline.[7] In Georgia, demand for industrial power is surging to record highs, with the projection of new electricity use for the next decade now seventeen times what it was only recently. A significant factor behind the surging demand is artificial intelligence, which is driving the construction of large warehouses of computing infrastructure that require exponentially more power than traditional data centers. AI demands massive cloud computing, further pressuring the nation’s aging electrical grid — the network of transmission lines and power stations that move electricity around the country.

Few individuals comprehend how much power AI consumes. Each AI server uses five to nine times more power than traditional servers and requires ten times more cooling. Nvidia’s new semiconductor chips will only increase this demand. Power demand in the U.S. has held steady for thirty years, but the AI boom will cause a significant surge in demand. This shift, alongside moving to ‘clean energy,’ will challenge the country’s sixty-year-old grid system. A single Nvidia graphics processing unit (GPU) consumes the same energy as a typical American home.[8]

Generative artificial intelligence may eventually transform many industries and the way people work. But a recent report that OpenAI chief executive Sam Altman is talking to investors about an artificial intelligence chip project that may require raising as much as $7 trillion raises questions. This amount equals the combined gross domestic product of Germany and the United Kingdom. A project seeking trillions rather than billions reflects the market’s euphoria over AI, the Nvidia chips that power it, and Microsoft’s cloud-based servers that host it.

The historical parallel of record-high AI-related stock valuations recalls the boom and bust during the dot-com bubble era when price dominated fundamentals. However, the market has apparently decided that Microsoft’s market value (7.1%) should exceed the combined index weights of the entire energy and utility sectors (6.2%), two sectors critical to the very existence of Microsoft and Nvidia. A passage from Benjamin Graham’s book The Intelligent Investor explains the speculator’s mindset:

Most investors, I think, use market price as the signal of whether they are right or wrong. If you buy and the price goes up, you’re “right.” If you buy and the price goes down, you’re “wrong.”

Price momentum attracts speculators, who may buy Nvidia and AI-related stocks because of soaring stock prices. The speculator believes that price indicates whether one is right or wrong, but using only price provides an incomplete picture. One purchases a stock for $100, which then jumps to $110. Does one believe they are right? The stock drops to $90, but now one must decide whether he is wrong or the market is wrong. If price is one’s only feedback mechanism, one might have to wait months or years to determine whether they were right. Instead, Benjamin Graham focused on “data and reasoning.” If an asset goes up, did it go up for the reasons one expected, based on the evidence one gathered? Being intellectually honest about whether one was right or wrong for valid reasons may be the most challenging aspect of investing.

Distinguishing between the probability of an event and the actual outcome is another challenge. A high probability does not equate with certainty. Markets are too unpredictable and too complex. A weather forecast for a 70% chance of rain is highly probable, but it does not mean it will rain. The outcome is still uncertain. The same principle applies to investing. Based on one’s analysis, the investor might determine that an investment has a high probability of success, but there are always variables that could shift the outcome. Understanding this difference is critical to successful long-term investing. The most likely events can fail to materialize; conversely, low probability but catastrophic events can and do occur.

The investor must prepare for various outcomes, including those that seem unlikely. In preparation, the investor should construct a portfolio that can withstand different scenarios, particularly unexpected ones. As Warren Buffett understands, financial markets will never unfold as predicted, and one should never underestimate risk. In Berkshire Hathaway’s 2023 letter to shareholders, Buffett wrote:

“Your company also holds a cash and U.S. Treasury bill position far in excess of what conventional wisdom deems necessary. During the 2008 panic, Berkshire generated cash from operations and did not rely in any manner on commercial paper, bank lines or debt markets. We did not predict the time of an economic paralysis, but we were always prepared for one.”

Because investors cannot predict the future, they must prepare, which means building a portfolio that can withstand the unknown. It also means maintaining ‘dry powder’ when the current opportunity set is limited. In the words of Charlie Munger, Warren Buffett’s late business partner, “I didn’t get rich by buying stocks at a high price-earnings multiple in the midst of crazy speculative booms, and I’m not going to change.” For ninety-nine years, Charlie Munger never predicted; he prepared.

[1] James Gleick, Chaos: The Making of a New Science (Viking Adult, 1987).

[2] Rusty Guinn, “The Three-Body Portfolio,” Epsilon Theory, December 27, 2017, https://www.epsilontheory.com.

[3] Murray Stahl, “4th Quarter Commentary,” Horizon Kinetics, January 2024, https://www.horizonkinetics.com.

[4] Leigh Goehring and Adam Rozencwajg, “The End of Abundant Energy: Shale Production and Hubbert’s Peak,” Natural Resource Market Commentary – Fourth Quarter 2022, February 28, 2023.

[5] Ben Inker and John Pease, “Magnificently Concentrated,” GMO Quarterly Letter – First Quarter 2024.

[6] James Stack, “Technical and Monetary Investment Analysis,” InvesTech Research, March 15, 2024.

[7] Evan Halper, “America is Running Out of Power,” The Washington Post, March 7, 2024.

[8] Freda Duan, “Where’s the Power?” X Corporation, @FredaDuan, February 23, 2024.