FRP Holdings is a real estate developer in Washington, D.C., and Baltimore. FRP’s largest real estate asset comprises five properties in southern Washington, D.C., in various development stages. The company also leases mining royalty land that generates almost $12 million in annual revenue from fourteen properties in the southeastern U.S. In May 2018, the Company sold its portfolio of industrial warehouses to Blackstone for $359 million. The sold assets represented 60% of the company’s revenue at the time, and proceeds have been reinvested over the past several years.

We find comfort in management’s record of intelligent capital allocation. The current CEO, John Baker II, has a history of acting opportunistically to build shareholder wealth, including through a $4.7 billion sale of FRP’s predecessor company to Vulcan Materials in 2007 and a $1.6 billion sale of an aggregates business to Martin Marietta in 2017. CEO John Baker (who also sits on Wells Fargo’s board of directors) has almost a 14% ownership stake in FRPH. At the same time, the Baker family, which has managed the company for generations, cumulatively owns nearly a third of outstanding shares.

FRP’s mining assets offer a unique and low-risk exposure to the aggregates mining business. Vulcan Materials, which maintains a close relationship with FRP and occupies 80% of FRP’s mining properties, has provided a positive outlook for the industry. Commentary from Vulcan’s management points to strong demand and pricing in the Georgia and Florida markets, where FRP’s mining assets are located. In addition, Cemex’s operations at FRP’s Lake Louisa site should continue to boost production volumes. The company’s mining royalties segment provides a low-risk revenue stream of almost $12 million annually on 90%+ operating margins. Additionally, there will be opportunities to rezone and redevelop the mining properties in the future. These “second-life” opportunities could unlock hidden value for shareholders.

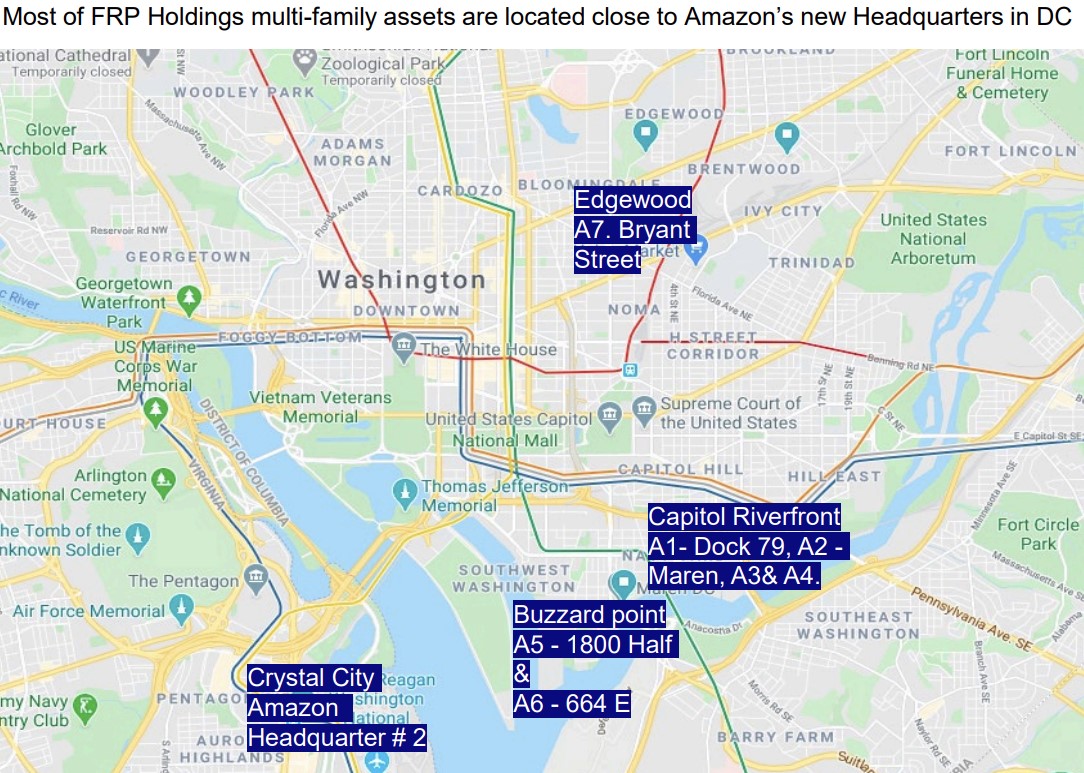

The company’s RiverFront properties in the Buzzard Point district of Washington D.C. generate strong shareholder returns. The properties were originally cement operations, but the company rezoned the land to build large multifamily buildings and one hotel. The first property, the 305-unit, 300,000-square-foot Dock 79, was completed in 2017, while the second property, The Maren, was completed in early 2020. More importantly, the Buzzard Point neighborhood is experiencing rapid growth. The RiverFront properties are located directly across Nationals Park and a short walk from Audi Field, the home stadiums of the region’s Major League Baseball (MLB) and Major League Soccer (MLS) franchises. FRP’s RiverFront assets are also an 8-minute drive from the future location of Amazon’s second headquarters in Crystal City, VA. Several other large residential and commercial projects are currently being developed in Buzzard Point. FRP has three remaining lots in the area that are expected to be developed, and the high growth rates in Buzzard Point should add value for FRPH shareholders.

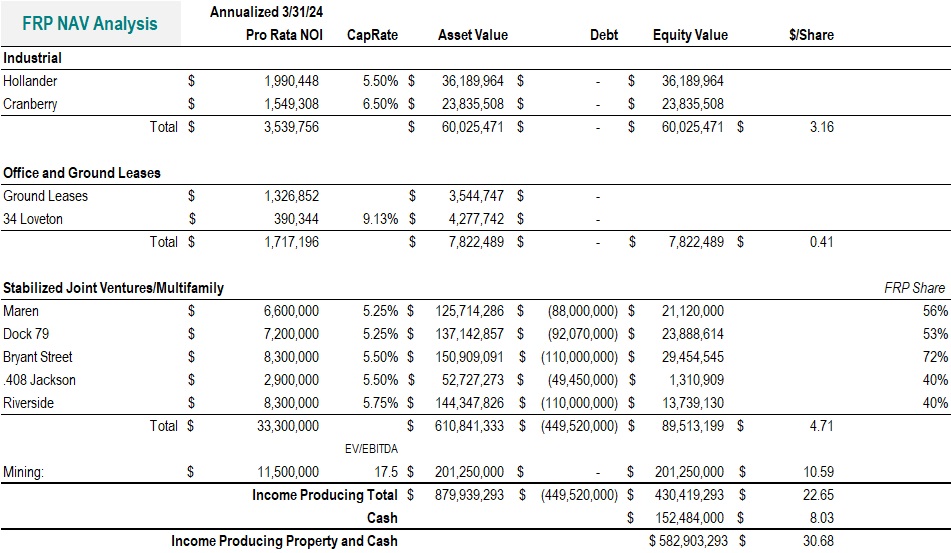

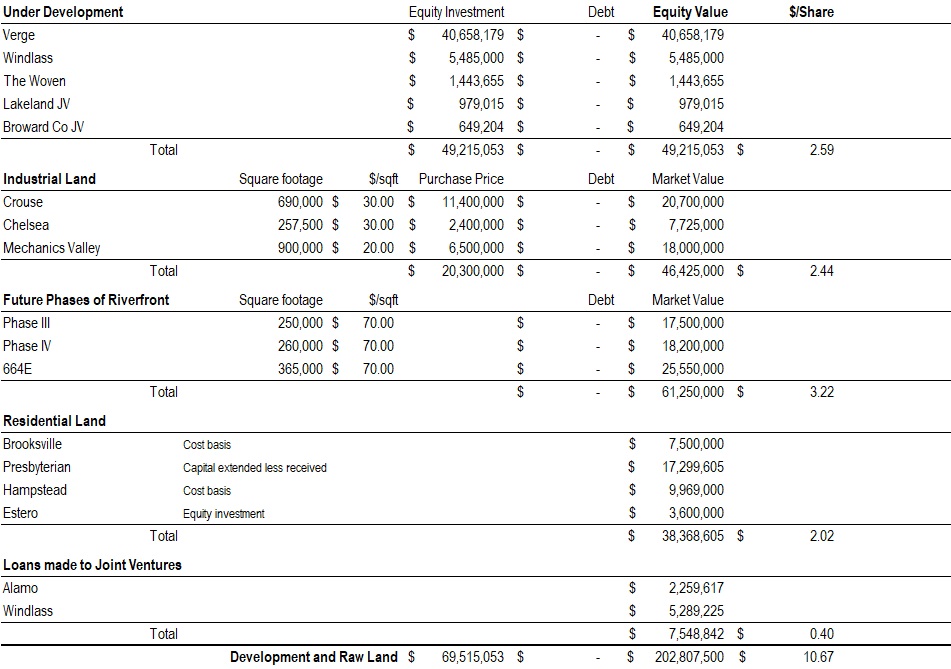

In valuing FRPH shares, we derive a net asset value (NAV) of $763 million, or $40.20 per share. Our estimate is very conservative given a relatively modest multiple for the mining royalties, no attribution of value to any second-life mining opportunities, and low premiums for various projects in early development. We see the most upside to our estimated NAV from Bryant Street and the remaining RiverFront properties. Regardless, our NAV of $40.20/share reflects a 32% premium to FRPH’s current market value.

FRP Holdings traces its origins to 1929 when Thompson Baker repurchased his father’s repossessed aggregates pit from a bank. In 1932, Baker joined Jim Shands, a competitor from Gainesville, Florida, to form Shands & Baker. Thompson Baker temporarily left the business in 1942 to join the Marine Corps in World War II but returned to Shands & Baker after the war. The merged company continued operations for decades and entered the trucking and hauling industry in 1962. In October 1972, Shands & Baker merged with two concrete companies to form Florida Rock Industries and went public. In 1986, Florida Rock Industries spun off the real estate and transportation assets into a separate entity called Patriot Transportation Holdings. At the time, the Baker family owned 44% of Patriot and held three seats on its board of directors. Patriot, the legacy company of the current FRP Holdings assets, began developing warehouses and industrial-use properties in the late 1980s. In January 2015, the company spun off its transportation and hauling assets as Patriot Transportation Holding and renamed the remaining company with the real estate assets FRP Holdings (FRP is an acronym for “Florida Rock Properties”).

Although FRPH was separated from Florida Rock Industries (“FRI”) in 1986, the Baker family maintained 25% ownership of FRI while also managing its operations. John Baker II, the current CEO of FRP Holdings, was the president of FRI, while his brother, Ted Baker, and nephew, Tom Baker II, also held managerial roles. In 2007, FRI was sold to Vulcan Material Company (“VMC”) for $4.6 billion in a cash (70%) and stock (30%) transaction. Following the sale, John Baker II joined VMC’s board of directors, while Tom Baker II joined as president of VMC’s Florida Rock division. During the economic downturn in 2009, both Bakers left VMC in search of a capital partner to finance a new business venture in the aggregates industry. This venture ultimately became Bluegrass Materials. In early 2017, Tom Baker II rejoined VMC as senior vice president after resigning his post as CEO of FRP.

The Baker family owns more than 32% of FRPH and has managed the company since it was founded by Thompson Baker in 1929. The CEO is John Baker II (age 75), Thompson’s son. John succeeded his nephew, Tom Baker II (age 60), as CEO in March 2017 when Tom rejoined Vulcan as a senior VP. John has an undergraduate degree from Princeton University and a law degree from the University of Florida. He originally joined FRP as an in-house lawyer before leaving in 1974 to join the Marine Corps (following in his father’s footsteps). John has previously served as CEO of Florida Rock Industries, including during a long tenure from 1996 until the business was sold to Vulcan in 2007. John was also instrumental in the successful Bluegrass venture. John has also been a member of the Wells Fargo Board of Directors since 2009. John was previously the CEO of Patriot (before FRP’s separation) from 2008 to 2010. John owns 1.38 million FRPH shares, representing almost 14% ownership in the Company.

Following John and Tom’s departure from Vulcan in 2009, the Bakers began searching for a capital partner to finance an acquisition in the construction materials sector. At the time, assets across the industry were selling at distressed prices as companies desperately sought to pay down debt burdens. In 2010, the Bakers partnered with Lindsay Goldberg (a private investment firm in New York) and Bluewater Worldwide to take advantage of the attractive asset prices. The partnership was called Panadero Aggregates Holdings, and its principal subsidiary was Bluegrass Materials. Bluegrass initially acquired various aggregates operations from Cemex for $90 million. Bluegrass grew with several bolt-on acquisitions until it eventually had operations from twenty-three locations across the southeastern U.S. The company was also the leading aggregates producer in Kentucky and Maryland. Bluegrass was sold to Martin Marietta Materials in 2017 for $1.625 billion in cash. After seven years, the partners reportedly recognized incredibly high returns of more than three times the original investment. While Bluegrass did not directly impact FRPH, it illustrates the Bakers’ skill in capital allocation.

John Baker II and his son, Ted Baker II (who continues to run Bluegrass), opportunistically acquired and sold assets at highly attractive prices when market conditions improved. This price sensitivity was also demonstrated in the sale of Florida Rock Industries to Vulcan. Reflecting on the 2007 FRI sale, John said, “We had no intention of selling. We were having a ball. We were making the most money we had ever made. One of the largest companies in our industry came to us and made us an offer we couldn’t refuse. I’ll never forget my brother and I walking out of that meeting. We both looked at each other and said we had no choice. While our family had a significant stake in the company, it was a public company, and we had to, in our view, sell it to be fair to the other shareholders.”

Along with the Bluegrass story, this demonstrates a strong shareholder orientation in management. These tendencies are critically important in the company’s redeployment of capital. In our view, John Baker’s managerial track record suggests that capital will be allocated intelligently. We acknowledge that these success stories point toward the Bakers’ capabilities in the aggregates mining business rather than in real estate development. However, the company’s real estate assets are managed by David deVilliers (age 72), who has been with FRP Development since its inception in 1989. It is based in the Baltimore region, where the company has a solid real estate track record.

We note that deVilliers also has an impressive managerial record. In addition to the high returns achieved on the RiverFront properties, deVilliers was instrumental in developing, leasing, and ultimately selling the industrial warehouse properties to Blackstone at a relatively strong cap rate of 5.6%. As another example, deVilliers successfully rezoned 74 acres at the Company’s Windlass Run Residential property and executed the sale of the property for $19.2 million, reflecting a gain of $11.2 million. These properties were sold in 2013 and 2015 when real estate assets were still coping with the aftermath of the recession. The proceeds were mainly used to buy other industrial assets, which were then sold to Blackstone as part of the larger asset sale.

On March 22, 2018, FRP announced the sale of forty-one industrial warehouse properties and three adjacent land parcels to Blackstone for $358.9 million, representing an implied cap rate of 5.6% on almost four million square feet of warehouse space. The transaction was massive, representing 60% of revenues and 65% of FRPH’s market capitalization at the time. The sold properties represented all the company’s warehouse assets, leaving three office properties in the Asset Management segment. The deal closed on May 21, 2018. After the sale, the company cut its Baltimore headcount from eighteen employees to nine for $1.5 million in annual savings. The transaction was eligible for a Section 1031 like-kind exchange to defer taxes on the realized gains. Still, the company did not find an acquisition opportunity suitable to management’s conservative standards. As the 180-day deadline for 1031 exchanges expired, the company incurred a $45 million tax on the realized gain of $165 million. The tax bill partially contributed to a gradual sell-off in FRPH’s stock price at the end of 2018.

Business

The company owns approximately 21,000 acres of land in Florida, Georgia, Maryland, Virginia, South Carolina, and the District of Columbia. This land is generally held by the company in four distinct segments: (i) Industrial and Commercial Segment (land owned and operated as income-producing rental properties in the form of commercial properties), (ii) Mining Royalty Lands Segment (land owned and leased to mining companies for royalties or rents), (iii) Development Segment (land owned or joint ventures held for investment to be further developed for future income production or sales to third parties), and (iv) Multifamily Segment (ownership, leasing and management of buildings through joint ventures).

The Industrial and Commercial Segment includes nine buildings at four commercial properties owned by the Company in fee simple as follows:

- 34 Loveton Circle in suburban Baltimore County, Maryland, consists of one office building totaling 33,708 square feet, which is 90.8% occupied (the company occupies 16% of the space for use as their Baltimore headquarters). The property is subject to commercial leases with various tenants.

- 155 E. 21st Street in Duval County, Florida, was an office building property under lease through March 2026. FRP permitted the tenant to demolish all structures on the property during 2018.

- Cranberry Run Business Park in Harford County, Maryland, consists of five industrial buildings totaling 267,737 square feet, 92.1% occupied and 92.1% leased. The property is subject to commercial leases with various tenants.

- Hollander 95 Business Park in Baltimore City, Maryland, consists of three industrial buildings totaling 247,340 square feet, 100.0% leased and 100.0% occupied.

The Multifamily Segment is invested in several stabilized multifamily joint ventures:

- Dock 79: In 2014, The company contributed 2.1 acres of the total 5.8 acres to form a joint venture owned by FRP (77%) and MRP Realty (23%). Construction commenced in October 2014 on a 305-unit residential apartment building with approximately 14,430 square feet of first-floor retail space. Lease-up began in May 2016, and rent stabilization of the residential units of 90% occupied was achieved in the third quarter of 2017. During the fourth quarter of 2022, the company sold a 20% interest in a tenancy-in-common of Dock 79, where FRP Holdings remains the majority partner with 52.8% ownership.

- The Maren: In 2018, the company and MRP Realty formed a joint venture to develop the second phase only of the four-phase master development known as Riverfront on the Anacostia in Washington, D.C. The joint venture is developing a 250,000-square-foot mixed-use development that supports 264 residential units and 6,758 square feet of retail. Lease-up commenced in March 2020, and rent stabilization of the residential units occupied by 90% was achieved in March 2021. The company held a profit-sharing arrangement of 70.4%. During the fourth quarter of 2022, FRP Holdings sold a 20% interest in a tenancy-in-common of The Maren, where FRP Holdings maintains 56.3% ownership.

- Riverside: FRP Holdings and Woodfield formed a joint venture to develop a 200-unit residential apartment project at 1430 Hampton Avenue, Greenville, South Carolina. The project is in an Opportunity Zone, which provides tax benefits in the new communities’ development program. The company contributed $6.2 million in exchange for a 40% ownership in the joint venture.

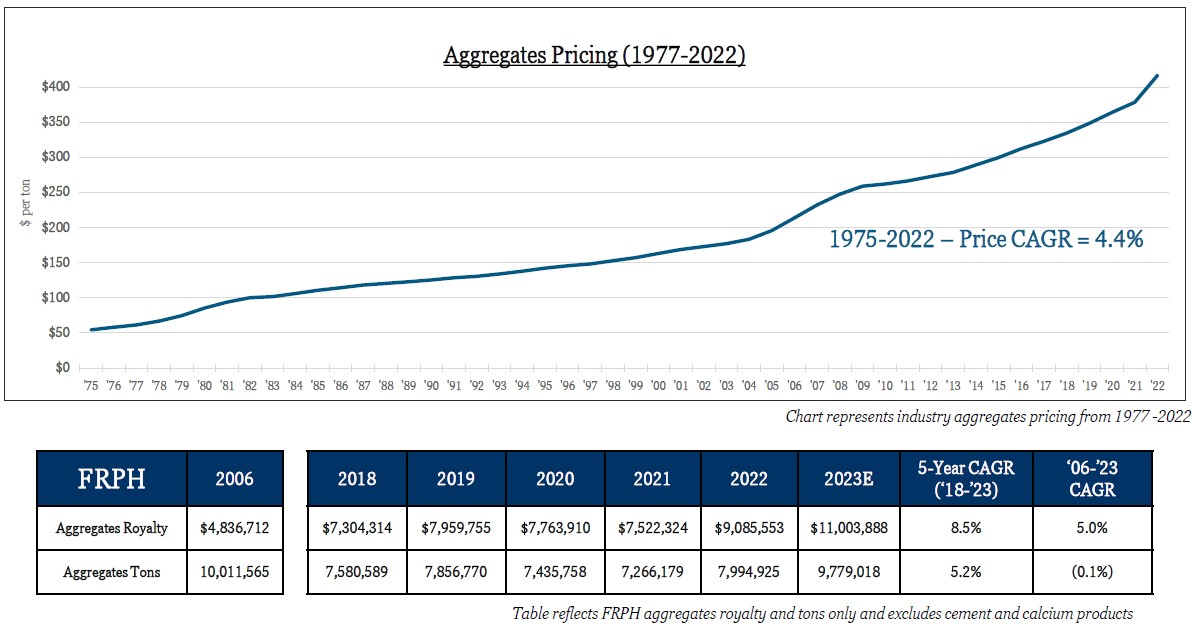

The Mining Royalty Lands Segment consists of a fee simple interest in fourteen open-pit aggregate quarries in Florida, Georgia, and Virginia, comprising approximately 16,650 acres. The company’s quarries are subject to mining leases with various tenants, including Vulcan Materials, Martin Marietta, Cemex, Argos, and The Concrete Company. Aggregates consist of crushed stone, sand, gravel, fill dirt, limestone, and calcium and are used primarily in construction applications.

Nine of the company’s quarries are currently being mined, and five of the company’s quarries are leased but are not currently being mined. The typical mining lease requires the tenant to pay the company a royalty based on the number of tons of mined materials sold from the mining property during a given fiscal year multiplied by a percentage of the average annual sales price per ton sold. In specific locations where the sand and stone deposits on the property have been depleted, but the tenant still needs the leased land, FRP Holdings collects a minimum annual rental amount.

The properties are occupied by companies mining for construction materials—primarily aggregates and cement. More than 80% of mining royalty revenues come from the company’s former Florida Rock Industry assets, which were sold to Vulcan Materials in 2007. Cemex and Martin Marietta are also large tenants. The aggregate business is highly cyclical; different geographic regions can experience different economics. Transportation costs to move aggregates from a quarry can quickly add up, even over modest distances. Hence, a quarry’s location near an area with growing development and construction needs is a significant competitive advantage for a mine operator. Vulcan, FRP’s largest mining tenant, frequently claims that “higher logistics costs widen the natural economic moat around our quarries” due to the relative proximity of Vulcan’s quarries compared to its competitors, which is a positive readthrough for FRP’s mining assets.

![]()

Despite these advantages, the industry is cyclical. During the extremes of the 2008-2009 recession, the company saw its mining royalties decline by 50% before eventually returning to normalized levels. FRP’s almost negligible exposure to cost risk should keep the segment generating positive cash flows, even amid a draconian scenario.

It is essential to consider commentary from Vulcan’s management for insight into expectations for FRP’s future mining royalties. Commenting on its Georgia operations, Vulcan’s management said, “We like what we see in Georgia . . . . The outlook on public spending and the backlog of work to be done bodes well. Pricing in that market has been very strong.” We also note that, in response to a question about growth drivers, management specifically cited “places like Georgia, Texas, or Florida, which have very good and growing highway programs.” Considering these comments, one can infer that FRP’s mining assets are largely in growth markets supported by public spending and that the Georgia properties should see more robust pricing.

FRP’s management often highlights specific second-life opportunities for its mining properties. The company has zoned 4,300 acres in Brooksville, Florida, for a mixed-use development, including 5,800 residential units, 600,000 square feet of commercial uses, and 850,000 square feet of light industrial uses. While cautious about placing any value on these second-life opportunities, given the uncertainty surrounding the timing and specifics of any deal structure, there is significant long-term value in place. Management has been discussing the Brooksville development for more than twelve years. Nevertheless, these developments continue to be potential catalysts that could unlock hidden value for shareholders in the future. For example, a comparable waterfront development near FRP’s Fort Myers property has commanded valuations of $0.5-$1.0 million per undeveloped lot, which suggests an undiscounted value of $50-$100 million for this asset alone.

Valuation

The company consistently redeploys cash from asset sales, real estate operations, and mining royalties into new assets, allowing management to exploit its knowledge and expertise. The asset classes of choice are mixed-use, industrial, raw land, existing buildings, and repeatable strategic partnerships located in core markets with growth potential. Though far from a conglomerate, FRP Holdings contains several business segments in different and unrelated facets of the real estate industry, including in-house projects and many joint ventures.

The aggregates segment is a great business. The unit economics of an average aggregate operation have increased dramatically over time. The confluence of supply and demand characteristics greatly benefits the economics of an aggregate operation. When valuing FRP’s aggregate properties, we focus on the company’s fifteen aggregate properties currently leased to tenants for varying periods. The Brooksville location in Florida is a 50-50 joint venture with Vulcan Materials. Because FRP owns its aggregate properties in fee simple, there are two elements to value: royalty received from tenants for using its property to extract minerals and second life, or the property’s value after aggregates are depleted and the property assumes another use.

To calculate the royalty’s value, we apply a multiple based on the quality of the operations and prospects. For a business of this quality, we are comfortable paying up to eighteen times enterprise value divided by OIBDA (operating income with depreciation, amortization, and depletion added back) minus maintenance capital expenditures or an earnings yield of 5.56%. The margins of this business are very high (about 93% OIBDA margins); there are no capital requirements; the pricing power can temper the cyclicality of demand; latent demand underscores the durability of current earnings levels and creates a source of revenue in the future; and population growth in Florida and Georgia was 43% and 37%, respectively, from 1990 to 2020, which is significantly above the 20% for the United States as a whole.

The second-life value of FRP’s aggregate properties is attractive. In particular, we focus on Fort Myers Quarry (1,907 acres in Florida) and Brooksville. After completing phases one through five of its plans for Fort Myers, FRP hopes to have up to 105 lakefront lots of one acre each. The lots should be marketable after 2028. The property is one mile from the airport, twenty-five minutes from the ocean, and about twenty minutes by car to significant population centers, notably Fort Myers (population of about 96,000), Cape Coral (217,000), and Bonita Springs (56,000). Five luxury housing developments exist in the area: Miromar Lakes, WildBlue, The Preserve at Corkscrew, Bella Terra, and Corkscrew Shores.

Miromar Lakes is a master-planned gated community featuring signature championship golf and 700 acres of freshwater lakes with beautiful white sandy beaches. At the high end, some properties recently sold for $4 to $5 million. Miromar Lakes is located within a sizeable developmental sprawl near Target and Costco and right near Florida Gulf Coast University. There’s no Costco, Target, or university near FRP’s prospective lots. WildBlue is a master-planned community east of I-75 and the Corkscrew Road corridor. This 2,960-acre development includes three expensive artificial lakes, a byproduct of the site’s prior use as a limestone mine. The community will feature 1,096 single-family homes and 40,000 square feet of retail space at full build-out. Lee County has been granted 488 acres of the parcel for a regional public park. At the high end, recent sales have fetched between $3.1 million and $3.3 million. WildBlue is just southeast of Miromar Lakes and southwest of RFP’s phases one through five.

Directly southeast of WildBlue, three developments – the Preserve at Corkscrew, Bella Terra, and Corkscrew Shores – are connected to the suburban sprawl around Miromar Lakes. More developments to the east include Verdana Village and The Place at Corkscrew. Of the three, Corkscrew Shores is the most high-end and rural. The average of the median sales prices is a proxy for FRP’s potential house value – about $837,000. Since FRP’s lots are so disconnected from other developments, we reduced this figure to $750,000.

Other than Fort Myers, FRP’s foremost medium-term second-life opportunity appears to be the Brooksville land, owned 50/50 by FRP and Vulcan Materials. Brooksville is approved for 5,800 residential dwelling units and over 600,000 square feet of commercial and 850,000 light industrial uses on 4,280 acres. Although zoning approvals add value, investors may have to wait until the lease expires in 2032 for second-life monetization to begin. We value Brooksville currently at about $10,000 an acre, which is about the current value of the land as rural agricultural land. The remaining potential second-life properties include 15,971 acres of mineral properties, including the remaining Fort Myers property. Time is on the side of these properties, and their second-life value could be substantial, but due to uncertainty and lengthy potential lease expirations, we will not value the 15,971 acres. Consider this a margin of safety built into our model.

To summarize, $201 million for the royalty, plus another $229 million for the company’s remaining income-producing assets, equals $430 million. We add cash of $153 million, and the company’s total value equals roughly $583 million. We assign zero value for the 15,971 acres of remaining second-life land. FRP Holdings’ current market capitalization is $571 million. Given the company’s remaining assets, the market is mispricing the rest of the business.

Company management acknowledges the JV and development complexity added to a conglomerate without a readily accessible investor base. These actions increased the gap between the company’s market price and its true worth. We believe management operates with good intentions, and the Baker family holds over 30% of the outstanding shares. The company has demonstrated a long history of success, and we are perfectly content to participate alongside the Baker family.

Risks

A decline in the economic conditions in Baltimore and Washington, D.C. markets could adversely affect FRP’s business. Nearly all their residential and mixed-use commercial properties are in the Baltimore area and Washington, D.C. Their operations may also be affected if too many competing properties are built in these markets. An economic downturn in these markets resulting from factors outside their control would adversely affect their operation. Such factors as the downsizing or relocation of government jobs, crime, or acts of terrorism could trigger such a downturn.

The company conducts a significant portion of its operations through joint ventures, which may lead to disagreements with joint venture partners and adversely affect FRP’s interests in the joint ventures. In each of their existing joint ventures, the consent of a joint venture partner is required to take specific actions and, in some cases, will share equal voting control. Joint venture partners and future partners may have interests that differ from FRP’s interests and may result in conflicting views on the conduct of the joint ventures.

The company’s business may also be adversely affected by seasonal factors and weather conditions. The Mining Royalty Lands Segment and the Development Segment could be adversely affected by reduced construction and mining activity during periods of inclement weather. These factors could cause operating results to fluctuate from quarter to quarter. An occurrence of unusually harsh or long-lasting inclement weather, such as hurricanes, tornadoes, and heavy snowfalls, could hurt operations and profitability.

Company revenues also depend on construction sector activity, which tends to be cyclical. Financial results depend partly on residential, commercial, and infrastructure construction activity and spending levels. The construction industry tends to be cyclical. Construction activity and spending levels vary across our markets. Interest rates, inflation, consumer spending habits, demographic shifts, environmental laws and regulations, employment levels, and the availability of funds for public infrastructure projects influence them. Economic downturns may lead to recessions in the construction industry, either in individual markets or nationally.