E-L Financial Corporation is a Toronto-based life insurance holding and investment company controlled by the Jackman family, which is now in its third generation of stewardship. They are beneficiaries of one hundred years of compounding with the 2023 centenary of the “E-L” piece – Empire Life Insurance Company, based two and a half hours north-east of Toronto in Kingston, Ontario. In addition to owning 99.4% of Empire Life, E-L runs its own $4 billion investment portfolio and controls 56% of the listed closed-end fund United Corporations Limited. These businesses are consolidated into ELF’s financial statements. Additionally, there are two associated companies, Algoma Central (37% owned) and Economic Investment Trust8 (25% owned).

E-L is remarkable—there are effectively fewer shares outstanding than when the company was formulated in its present state in early 1970. The Jackman family has a reputation for parsimony. Still, the most significant advantage for shareholders is that their most incredible area of thrift is arguably in the issuance of shares of their companies. This is a long-term observable trait across the three Jackman companies of interest, making Warren Buffett seem almost profligate in equity issuance. That the Jackmans have started to retire equity since 2020 magnifies this attribute.

The first Jackman generation, led by Henry R. (Harry) Jackman, became involved in the securities industry at Dominion Securities in the 1920s alongside Charles P. Fell. Fell left in 1929 to “straighten out” Empire Life. Over the next thirty years, Harry Jackman spent nine years as a Canadian MP but acquired control of several closed-end funds, most notably the then publicly traded Dominion & Anglo Investment Corporation Limited, ELF’s most significant (41%) shareholder. In 1956, Harry joined the Empire Life board, became chairman in 1957, and acquired substantial interest from Fell in 1959. In the meantime, Harry’s son, Henry N.R. (Hal) Jackman, had commenced an investment career that saw him increasingly interested in Empire Life.

Empire Life Insurance Company was formed in February 1923, and in August 1929, having built assets to $699k, effectively acquired Commonwealth Life and Accident Insurance (assets $621k) to enlarge the company. Fell became President of Empire Life in March 1933, a position he held until February 1967. Empire Life acquired Mutual Relief in 1935. In partly paid form, Empire Life shares were unlisted but tradeable via brokers until October 1951, when its reorganized 32,024 shares of par value $10 were listed on the Toronto Stock Exchange, with early trades at $19. The company rode an astonishing wave of growth in life insurance post-war, which took Canadian life insurance premiums to over 3% of GDP.

Empire’s premium income grew at over 10% per annum for seventeen years, constantly adding to a pool of assets on which an average of 5.2% per annum was earned (the assets were mainly bonds). A conservative approach to dividends and no new share issuance other than stock dividends and stock splits resulted in a significant compounding of per-share value by 21% per annum over the seventeen years. Henry Jackman’s significant shareholding was joined by his son, the current patriarch Hal Jackman, by the late 1960s, when they had jointly acquired 47% of Empire’s shares. The means of obtaining these shares was via control/influence over several (then) listed closed-end funds, most of which have been de-listed.

In November 1968, Empire became the first Canadian life company to own more than 20% of the shares of another corporation. In November 1968, Empire offered its shareholders four new shares of E-L Corporation, plus a single warrant to purchase ELF at $12 in exchange for every two Empire shares. With the Jackmans in control, the offer rapidly gained acceptance, and by January 1969, Empire was a 90% subsidiary of ELF. Empire Life’s 706,034 shares in late 1968 became, after the full warrant exercise, 1.765 million ELF shares. The Jackman family had a strategy: in January 1969, they agreed to acquire control of Dominion of Canada General Insurance (Dominion) with a scrip offer by ELF of three convertible preference shares, seven common shares, and a $12 warrant per Dominion share. They were effectively gaining 10-1 leverage on Dominion’s 202,000 common shares.

On conversion of the preference shares (and warrants from both Empire and Dominion transactions), these would be the last new securities of any note issued by E-L Financial to the present day. With recent capital management initiatives, ELF has fewer outstanding shares than in 1971. With minimal share issuance between 1923 and 1951 for Empire Life, no share issuance between the public listing in 1951 to the ELF transaction in late 1968, and the two warrant issues plus script bid for Dominion, the exercise in 1969 is the only new equity ELF and its predecessor has issued in a century. Considering that the equity issued to buy the entire Dominion company was worth $25 million in 1968, Dominion stripped its life company (estimated 20% of value) and sold it to Travelers for $1.08 billion in November 2013.

ELF further developed the insurance business in 1986 by acquiring Montreal Life from Guardian Royal Exchange in a creative transaction that involved issuing no holding company securities but allotting GRE 19% of a subsidiary company holding the enlarged life business. Empire Life was subsequently supplemented with books of business from other life insurers and with two small acquisitions. E-L bought out GRE in December 2015 at approximately book value (19% for $199.9 million) and increased the effective ownership of the enlarged Empire back up to 99.3%. Empire Life has been able to finance itself with a series of preference share issues listed on TSX until 2021, although ELF entirely holds the only residual series ($100 million) remaining. In 2021, Empire Life issued a Canadian insurer’s first limited recourse notes and continued using subordinated debentures.

Empire’s business has not changed radically in some years. The company has three key areas: Wealth Management, comprising segregated funds of some $8.5 billion and annuities of $850 million; Group Solutions; and Individual insurance, the longest-standing component of the company. The wealth management business is a management fee-driven division with management fees derived for the investment management of the segregated assets – effectively investments with some form of death benefit guarantee or guaranteed minimum withdrawal benefit; insurance contracts make up 95% of the segregated fund business. This business has significant equity market exposure, with over 70% of assets in preferred and common stocks at the end of September 2023. Naturally, the company is directly sensitive to equity market levels concerning fees but also drops in times of equity market dislocation.

Group Solutions focuses on small to medium-sized companies offering benefits such as dental, assorted medical, accidental death, and more niche products in travel assistance. The market for these products is consistently competitive, and the expected profit from in-force business of $25-$30 million per annum has been eroded in the past two years by adverse claims experience, including internal issues related to staffing. Despite pulling in over $450 million of premium income, the division is barely profitable, with an expense-to-premium ratio of over 25%.

Individual insurance—term life and universal life—has expected profits per annum of $50 million; however, recent results have been volatile due to changing interest rates (favorable when rates rise as discounted liabilities fall) and changes in claims and especially lapse rates, a fundamental issue for insurers worldwide. However, the business continues to generate slow but steady premium growth at $450 million per annum and, under normal conditions, is highly profitable given the substantial investment backing to policies.

Empire is Canada’s ninth largest life-based company, measured by assets but only eleventh by premiums. There are four significant life insurance-based companies publicly listed in Canada. All have specific angles with significant non-Canadian operations. The nearest real comparative in the publicly listed sphere for Empire is iA Financial (IAG.TO). This CDN $9.2 billion market capitalization business has a U.S. operation but is still dominated by its Canadian business, similar to Empire. Not surprisingly, in keeping with the ethos of ELF, Empire Life stands out as an asset-rich, modest-growth company against the giants of the industry. However, it has been consistently profitable and been an attractive dividend payer to ELF since the 1968 reorganization. As a guide, since 2010, Empire Life has paid out $550 million in dividends to ELF, including $75 million in 2023. Most notably, when ELF commenced its equity retirement program in March 2020, the first tranche was funded by Empire’s declaration of a $113/share dividend in late February 2020 – yielding $111 million to ELF.

On 30 September 2023, Empire had a net worth of $1.74billion (including $100million preferred stock, all held by ELF) and capital notes; removing the preferred capital notes and $87 million of intangibles gave Empire a tangible book value on 30 September 2023 of $1,357million ($1,377 per Empire share of which there are only 985,076 being 99.4% owned by ELF). Adding the disclosed contractual service margin on a pre-tax basis of $1,567 million would give an adjusted book value of $2,924 million. Allowing for goodwill would boost this to just over $3 billion.

We have compared the four largest publicly listed entities with Empire. Using metrics at a discount to the lowest publicly listed cohort (IAG) would price Empire at $2,140 – $2,672 per share or $2,108 – $2,632 million. This is somewhat greater than prior estimates; we have used ~1.88 billion for the common equity of Empire to support a higher valuation of ELF. We average the two methodologies and use a gross value of $2,350 million for Empire.

United Corporations Limited (UCL) is a CDN $2 billion closed-end fund established in 1933 from the remnants of Consolidated Investment Corporation, which defaulted on its loan commitments. The entire history of UCL, with every year’s equity base, adjusted NTA, and stock dividend, is laid out in each year’s annual report. The entire stock portfolio is disclosed each quarter. We separate UCL when valuing ELF. UCL is a global investor with three external managers – Comgest Asset Management (Dublin) with $550 million, Causeway Capital Management (Los Angeles) with $500 million, and Neuberger Berman Canada with ~$1 billion having been allotted an approximate quarter tranche of assets from the displaced manager, Harding Loevner. UCL has a 9.4% shareholding in Algoma Central (ALC.TO), a 27.8% direct associate of ELF, but which accounts for only ~2.6% of UCL’s assets.

ELF’s involvement with UCL began in May 1972 when they acquired a 13% block of shares at around a 17% discount to net asset value. ELF built the stake up over 40% by 1976 as the share price of UCL fell in line with equity market distress. ELF’s stake remained at just over 40% for some thirty years before it was built to 46% in 2008 and finally consolidated with over 50% in the final quarter of 2012. A Jackman-related company, United Connected Holdings, owns 2.7 million shares. UCL has historically traded at a significant discount to NAV – currently around 37% – despite recent share buybacks. This reflects the extraordinary portfolio diversification with 730 stocks as of 30 September 2023; UNC is a cost-effective (0.6% annual fee before stock lending income) vehicle for global equity exposure. ELF controls 56.6% of the capital and the Jackman-related company a further 24.4%, leaving a free float of only 19% (2.1 million shares) or ~$260 million of equity capital. In tandem with ELF, UCL has made six equity retirement initiatives since March 2020—similarly, four “normal course issuer bids” (on-market buybacks) and two “substantial issuer bids” (off-market tenders), retiring 7.6% of 2020 capital at a 39% discount to the current net tangible assets.

Valuation

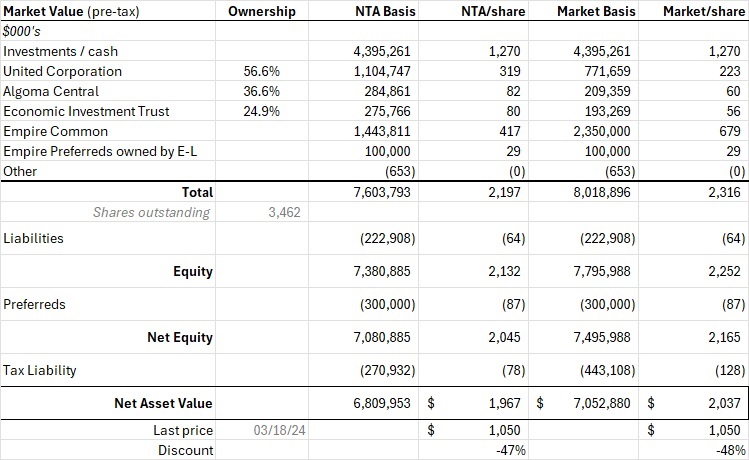

E-L Financial is a relatively simple deconsolidation of Empire Life and UCL, then valuing these entities separately; we add other investments at market value, even though significant discounts are involved in the closed-end fund companies. E-L Financial, excluding UCL or other related investments, has a diverse common and preferred stock portfolio of just under $4.2 billion on 30 September 2023. We have made assorted adjustments to the valuation to account for the substantial issuer bid in November in both ELF and UCL. We do NOT adjust for EVT’s circular shareholding in ELF, which would further increase the value per share.

Our two sets of valuations coalesce to a degree; valuing everything at net tangible assets brings down the value of Empire while carrying UCL at some $300 million (~ $87/share) above its public market price. The reduced value of UCL and EVT to account for the public market discount is offset by the increased value – even allowing for an increased assumed tax impost – for Empire Life. Our tabulations, as of 31 December 2023, allowing for recent share buybacks and some investment gain in the parent in Q4 2023, are given below:

At the current price of $1048 at the end of December 2023, we view E-L Financial as trading at a 47% discount to a reasoned current value of the company, with an increased chance of the value emerging over time. We noted earlier that ELF has fewer shares outstanding today than in 1971. Since early 2020, ELF has disregarded its long-standing policy of not buying back shares and has completed six equity retirements. The six completed equity retirements have seen ELF acquire 13.5% of the capital outstanding before the announcement, at a discount of 40% to the 31 March 2020 quarter’s NAV (the recent low point) or at a 56% discount to the last disclosed equity value per share of $1,792 on 30 September 2023. The equity retirement is at a 60% discount to our mid-point valuation of $1979 per share. Few other capital allocation decisions add so much value – if only more shares could be acquired!

The end game might reasonably be to “own the last ELF share not owned by a Jackman.” The third-generation Jackman – Duncan – is now the Chair of ELF. The free float of ELF is gradually dwindling with Hal Jackman – now aged 91 and quietly leaving the board at the 2023 AGM – being “related” to 2,945,765 shares, either directly through a trust structure established in 1969 with his father or other companies in which he has an interest. Most of these shares are held in the two old closed-end funds (Dominion and Anglo Investment Corp and Canadian & Foreign Securities) and Ecando Investments and Dondale Investments. However, 11.2% of ELF is held in the Economic Investment Trust. That leaves only 515,959 shares or 14.9% of ELF in ‘independent” hands or $550 million trading but arguably over $1 billion of value.

In our view, the key to any end game is that it would be most unlikely to see a takeover offer by one group company for another. While it would appear logical for ELF to bid for EVT, the shareholders of EVT would not want the tax consequences. Such a bid would likely violate Canada’s tax-free share rollover legislation since the two parties would not be dealing at arm’s length given the 85% and 86% “influence” held by Hal Jackman before such a potential transaction. So, the end game, should the Jackman’s wish to privatize the bulk of the ELF group, realistically must go through equity retirement on an ongoing basis with a final “swoop.” While the substantial issuer bids (tenders) have amassed ~100,000 ELF shares on their three occasions, there are potential tax issues for acceptors, particularly foreign holders.

The best way forward for most investors would be a more aggressive market buyback and an agreed-on-market offer by the company. Based on recent experience, if done annually, it might only be three to four years before a small number of shares remain outstanding unrelated to the Jackmans. An NCIB, done as a maximum of 5% of outstanding shares, could eliminate these shares. With a low free float and enormous discounts to NAV, the opportunity cost of waiting in ELF is very modest.

Why would the Jackmans even want to privatize the group? There is significant trapped value in the form of hefty discounts to the value of liquid, globally traded securities that could be sold exceptionally quickly, which would accrue in some manner to the family, not necessarily at great expense to external shareholders. There are administrative savings from taking ELF and EVT private, though Empire would continue to lodge public accounts. Removing EVT and ELF from public markets would enhance the privacy the family craves. This family-controlled public company NEVER does presentations to shareholders, albeit the quarterly disclosure is exemplary.

In many ways, E-L Financial is the archetypal closely held family-controlled entity: if you invest, you do have to go along with the family at their pace. The good news is that from 2020 onwards, the equity retirement strategy of a group that has been tight with equity issuance in the first place is stepping up the pace – just a little.