Altius Minerals is the world’s premiere non-precious metals royalty company. Altius manages two complementary businesses: royalty investment and project generation. Royalty investment is the acquisition of royalties in producing mines. A royalty is a type of financing in which the investor buys the right to earn a percentage of a mine’s production. The royalty holder gets a payment “off the top” or before any expenses are taken out for the operation of the mine. In other words, royalty holders like Altius get paid before anyone else. If a mine produces, the royalty holder gets paid. Royalties are forever. As long as mines keep producing, Altius will continue to earn royalty revenues. Some of its potash royalties are in mines that have produced potash for hundreds of years. Altius also holds royalties on producing copper, iron ore, nickel, cobalt, zinc, gold, silver, and coal for electricity and steelmaking.

Project generation is the investment of small amounts of capital in dozens of mining prospects, which may or may not one day become mines. This was the company’s first business. It invested $600,000 in a uranium mining prospect, eventually selling its interest for over $200 million. Today, it holds dozens of these small investments, many represented by stakes in publicly traded mining companies in its equity portfolio.

St. John’s, Newfoundland-based mining prospect generation and royalty creator Altius Minerals has one of the best business models in the world. Altius is not a mining company. It does not produce commodities by operating expensive machinery and managing employees. By contrast, Altius collects royalties from the companies that operate and mine the metals and minerals. Altius’s team of geologists finds mineral-resource prospects. Then, the company finds a partner company to fund the capital necessary to drill and prove there are enough resources in the ground to mine, thereby earning its way into a significant ownership stake. Altius makes money in different ways from each deal, but the company always retains a royalty interest on the property. If a mine is built on the property, Altius’ royalty interest will typically generate 1%-3% of the proceeds from the mine’s production each month – with no further investment required.

A royalty creator like Altius is the best way to invest in commodities. Altius spends very little on any project and can sometimes generate an enormous return on its investment. The company invested about $2 million in November 2009 in its Kami iron ore discovery in eastern Canada. With Kami surrounded by existing mines, the odds were excellent that a new mine would be built on Altius’ discovery. The agreement resulted in the restructuring and financing of Alderon Iron Ore, which fulfilled its option agreement terms with Altius to earn 100% interest in the Kami iron ore project. Altius owned a significant equity position in Alderon and was a lender in concert with Sprott Resource Lending, with Altius lending roughly US$2 million of the US$14 million loan facility.

Alderon went through receivership in 2020, and at the end of that process, Champion Iron Limited acquired the asset following a competitive bidding process. Altius received 600,000 Champion Iron shares as consideration for the sale of its portion of secured debt and, in 2023, received an additional cash distribution of approximately $3 million. Altius retains a 3% gross sales royalty, which comprises an interest in land and follows the Kami project into the hands of any purchaser from the receiver.

The estimated pre-tax Net Present Value (NPV) at an 8% discount rate was US$1,698 million based on an average production rate of 7.8 million tonnes per year of iron ore concentrate at a grade of 65.2% iron over the life of the mine. The post-tax IRR for the project came at 18.3%, with a payback period of 4.9 years. Champion Iron has announced its plans to revise the project’s scope in an updated Feasibility Study, including Kami’s capability to produce Direct Reduction grade pellet feed. All that comes from an investment of just $2 million.

Altius also buys existing royalties from other royalty investors. Twenty years ago, Altius purchased a 0.3% royalty on all the nickel production at the Voisey’s Bay mine on the coast of Newfoundland. It paid $13.6 million and has received over $50 million in royalty income since. That investment paid Altius about $2.3 million over the last twelve months alone. The cash flow from the Voisey’s Bay royalty has made Altius much more attractive than most small mining and exploration companies, and it provides one of the critical underpinnings to its net asset value. The Voisey’s Bay royalty paid for itself years ago. The current mine life is estimated beyond 2034, so it’ll likely produce income for another decade or more.

In December 2013, Altius Minerals purchased a 51% stake in eleven royalty streams for $233 million from Toronto-based miner Sherritt International. The royalty streams come from eleven coal and potash mines in the Canadian provinces of Alberta and Saskatchewan. Altius also purchased Sherritt’s 50% stake in the Carbon Development Partnership (“CDP”). The CDP owns 7.2 billion metric tons of coal and 2 billion metric tons of potash in Alberta and Saskatchewan (1 metric ton = 2,200 pounds). The CDP also owns royalties on coal and potash production in the region.

To understand how this company patiently deploys capital, consider the company’s actions in 2008, when almost all asset prices dropped precipitously. During this crisis, Brian Dalton and his team at Altius had over $160 million in cash and a single royalty, generating several million dollars a year to operate the company. They sat down and listed all the best royalties they wanted to own. The Sherritt coal and potash royalties made their list’s top three most desirable assets. By July 2009, Altius completed its research on Sherritt. This was its top choice based on its quality, diversity, and longevity. Altius noted, “The royalties being acquired represent some of the highest-quality royalties available.”

In addition to the five coal royalties Altius purchased in the transaction, the company also acquired six potash royalties from Sherritt. Like electricity, potash is a necessary commodity for modern society. It’s the world’s third-most widely used crop and plant nutrient, after nitrogen and phosphorus. Potassium in potash increases water retention and crop yield per acre of land. It also improves food crops’ nutritional value, taste, color, texture, and disease resistance. It’s used in various fruits, vegetables, rice, wheat, other grains, sugar, corn, soybeans, palm oil, and cotton. Mankind needs potash to survive.

High-quality, profitable, well-financed public companies pay the potash royalties. They are well-managed companies and will remain excellent royalty-payers for decades to come. These are the best potash royalties on the planet and some of the best royalties of any kind. Canadian potash is a world-class asset. Canada produces about 40% of the world’s potash. Altius is buying royalties on roughly half of Canada’s potash output. Altius and its partners own a royalty on 20% of the world’s potash. The second and third-biggest potash-producing countries are Russia and Belarus.

Notably, one must note that these are royalty streams, not equity interests. Royalty holders do not pay the capital costs necessary to maintain and expand the underlying coal and potash mines. Mine owners do that. And royalty holders do not pay the operating expenses required to run the mines. Mine owners do that, too. Yet royalty holders still get their share of the revenues. There is no more efficient way to invest in a mine than to own royalties on its production. Furthermore, all the mines are in Canada, a competitive advantage. Some might see Altius’ tight geographic focus as a lack of sufficient geographic diversity, but geology is a complicated science. If one operates worldwide, gaining subtle but essential insights from focusing on one area is more difficult. Altius’ focus in Canada also means it carries less political risk than with royalties and other investments in mineral-rich but riskier places, like Africa, the Middle East, and Asia. There is arguably less political risk in a stream of royalties on mines in Canada than in almost any other country.

In addition to the potash royalties, Altius purchased Sherritt’s 50% interest in the Carbon Development Partnership (“CDP”) for $21 million. The CDP acquisition comes with 900,000 hectares of land, roughly 3,500 square miles, or the size of Delaware and Rhode Island combined. Some CDP land is near existing mines. The area’s geology for CDP and the Sherritt royalty lands is well-known.

Gold royalties are the envy of the investment world. By contrast, one’s eyes glaze over when discussing nickel, coal, or potash royalties. The most respected analysts believe that the large gold royalty companies are worth about twenty times their annual royalties. Altius purchased the Sherritt coal and potash royalties for just nine times royalties, a fair price for a great asset. One dollar of royalty income is one dollar of income. It does not matter if it comes from coal, potash, or gold. There is no rational reason to pay up for a high-quality royalty and permanently refuse to pay up for an equally high-quality royalty on another commodity.

Altius is a world leader in prospect generation. For every dollar Altius has spent on its prospects in the past ten years, its partners have paid more than $23. Each dollar Altius spent has generated investment profits of more than $13. Altius operates a highly efficient business model. As a prospect generator, Altius hands more than 95% of its investment risk over to a willing joint-venture partner and collects thirteen times its money in profits. Altius’ prospect-generation business is in better condition than it has ever been. Because of the 2011-2016 bear market in natural resources, Altius increased its land holdings from less than 500,000 hectares (about 1.2 million acres) to around 2.5 million hectares (about 6.1 million acres). It has mineral rights and joint-venture agreements in Canada, the United States, Chile, Ireland, and Australia.

In April 2015, Altius paid its first dividend of $0.02. In 2023, it paid a $0.08 quarterly dividend. The dividend at this level is sustainable and capable of growth. Altius is becoming a solid dividend-paying royalty company today. Still, another piece to its business has resulted in substantial investment gains and could easily continue to do so in the future. In addition to investing in existing royalties, Altius also creates royalties. This part of the business is called prospect generation/royalty creation.

Altius’ team of top geologists stake out original mineral prospects for a small amount. Then, they find a partner willing to earn a percentage of the prospect by taking on the financial risk of drilling enough holes to outline a full-blown mineral deposit. Altius then earns a royalty on the eventual production from that deposit. This business can be highly lucrative. It makes money without taking on much risk. It leaves all the risk to its partner. The prospect-generation business generates incredible returns on invested capital because Altius invests only a small amount of money in each prospect and then finds a partner to spend the bulk of the capital needed to develop the prospect. As of December 2023, Altius has seventeen exploration projects in various stages of development.

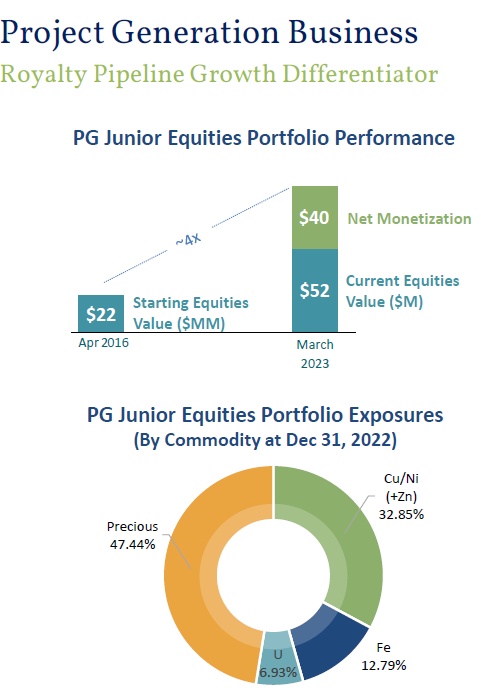

Altius’ project generation strategy is simple but requires a longer cyclically based strategy than most of their industry peers. Altius organically assembles and generates prospective geological real estate around the globe during periods of bear sentiment when capital for most is sparse. Hence, competition is light. On December 31, 2023, the portfolio value stands at $45.1 million. In 2023, Altius purchased new public equity investments totaling $1.6 million, while sales of public equities were $1.2 million. New equities are frequently added to the portfolio primarily from vending new projects the group generates in exchange for equity stakes.

Altius’ market cap is around C$810 million in January 2024. The company’s current intrinsic value is around C$1.2 billion. In the long term, given the size of the diversified mining market, we believe that the company is potentially worth several times its current intrinsic value.