The oil and gas industry loosely operates in three separate spaces: upstream, midstream, and downstream. Upstream exploration and production companies find and extract oil and natural gas, while downstream companies process hydrocarbons and turn them into valuable products like fuel and petrochemicals. Upstream and downstream companies make money in slightly different ways. Still, each tends to be boom and bust because they both earn a commodity-based margin, which is heavily influenced by the market prices of said commodities. Midstream companies behave more like a subscription business than a commodity-dependent cyclical.

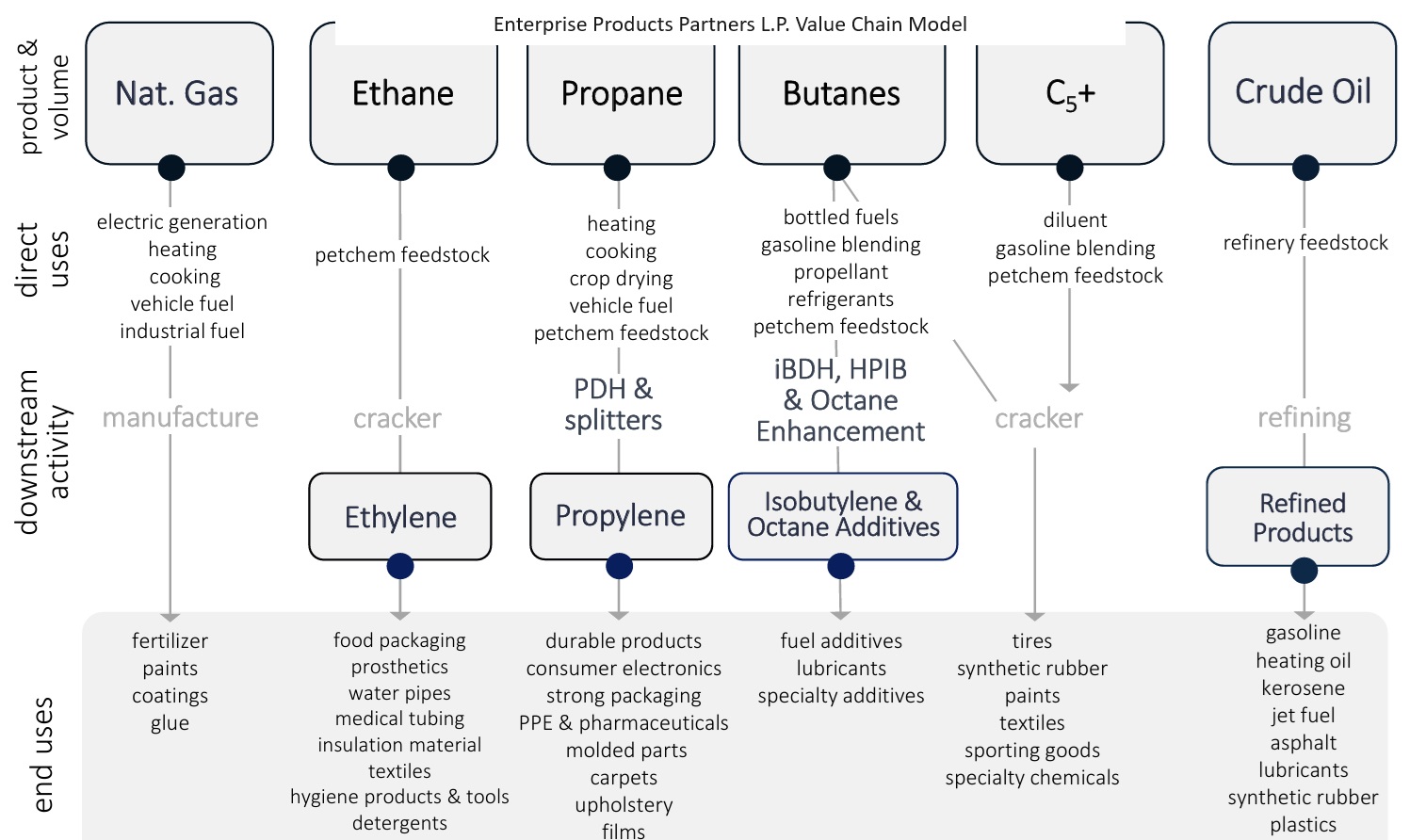

Enterprise Products Partners L.P. provides midstream energy services to producers and consumers of natural gas, natural gas liquids (NGLs), crude oil, petrochemicals, and refined products. It operates in four segments: NGL Pipelines & Services, Crude Oil Pipelines & Services, Natural Gas Pipelines & Services, and Petrochemical & Refined Products Services. Enterprise Products Partners L.P. was founded in 1968 and is headquartered in Houston, Texas.

Investment Thesis

Geographical and asset diversity allows Enterprise Products Partners to pursue growth in nearly any economic environment. The company can aggregate the supply of every type of hydrocarbon from multiple sources in major producing basins and deliver it to various end markets such as refiners, petrochemicals, and exports. Its vital marketing operations let it clip transaction-fee-like earnings during volatile oil and gas markets, as seen with winter storm Uri in 2021. Enterprise placed $3.5 billion of projects in service in 2023 and looks to invest a similar amount in 2024, providing solid volume growth and new fees.

The company has established a dominant position in natural gas liquids (NGLs), supported by a strong petrochemicals unit that converts low-cost U.S. molecules into more valuable U.S. exports overseas. Enterprise was years ahead of its peers in recognizing the opportunity and built a sizable but somewhat underappreciated business. This means it will be the primary beneficiary of U.S. NGL exports increasing in the coming years as international markets recognize the structural advantages of cheap U.S. feedstock. Enterprise has numerous attractive investments on the way, including its second propane dehydrogenation plant, which entered service in the second quarter of 2023, ethylene export expansions in 2023 and 2025, and an ethane export terminal in 2025.

With U.S. producers focusing on generating cash flows versus growing production at all costs, the U.S. midstream space has also had to adapt. Most U.S. midstream firms have concentrated on short-cycle efforts that can generate returns within eighteen months, including expansions of existing pipelines. The Navitas purchase for $3.25 billion in 2022 looks solid, as Enterprise is capturing substantial upside with the rapid near-term growth expected from Permian Basin natural gas.

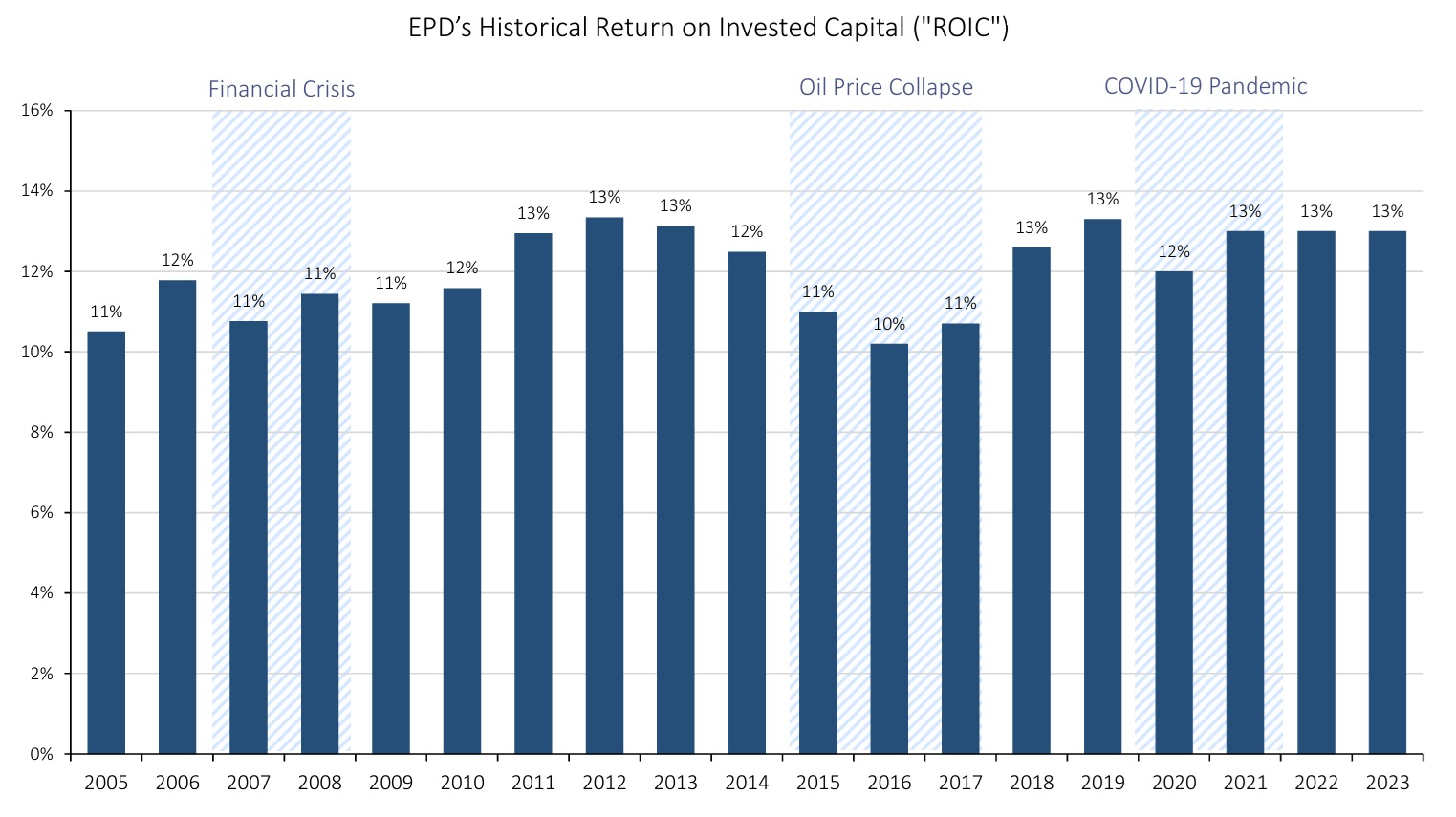

Returns on invested capital should average about 12% over the next five years, well above the company’s cost of capital of around 9%. Enterprise is a highly diversified master limited partnership, with operations in natural gas liquids (54% of gross operating margin), crude oil (18%), natural gas (12%), and petrochemicals (15%).

While Enterprise’s assets provide a strong competitive advantage on a stand-alone basis, its export assets across natural gas liquids and oil are critical contributors to extending its competitive advantage over a longer time frame. Enterprise was among the first to recognize the value of U.S. exports to international markets and has been a leader since the market first developed in the mid-2010s. Key to its advantage is ownership over every part of the natural gas liquids value chain, allowing it to direct molecules to Enterprise assets and capture fees at each step, including for export. For natural gas liquids in particular, these assets have allowed Enterprise to access high-priced international markets demanding cheap U.S. natural gas liquids feedstock versus being constrained to U.S. domestic markets. The International Energy Agency (IEA) projects that global demand for natural gas liquids will increase until 2050. Because natural gas liquids are a byproduct of natural gas production, the U.S. has enjoyed an NGL feedstock cost advantage for over a decade. Enterprise has numerous attractive NGL export investments, including ethylene export expansions in 2025 and an ethane export terminal in 2025.

Midstream companies create a competitive advantage by operating with scale and generating operational efficiencies. Efficient scale refers to situations where companies are effectively serving a minimal market size, and potential competitors have little incentive to enter the market because by doing so, they would lower the industry’s returns to below the cost of capital. While the midstream industry is massive, individual companies connect a limited number of markets. Therefore, their underlying routes can be considered separate, localized markets to which efficient scale applies. Even though low-cost shale oil and gas production in North America has increased, there is little evidence of speculative capacity additions, with most of a pipeline’s takeaway capacity being contracted before starting construction, ensuring that new capacity is added efficiently.

Midstream markets exhibit several characteristics of efficient scale markets. Demand for oil and gas products is growing slowly and should peak within the next decade or two, discouraging potential new entrants. Incremental demand can be met by incumbent companies at a meager cost, typically via compression, pairing or twinning a pipeline, making it difficult for new entrants to see a profitable investment opportunity. Demand is also inelastic for oil and gas, meaning potential new entrants cannot simply undercut existing operators on price to gain market entry. There are also significant barriers to entry regarding multi-billion-dollar investments to build new pipelines and related investments and satisfying regulatory and other stakeholder concerns, which have only increased in recent years. Finally, exiting the market is extremely difficult, as assets can operate for decades safely with minimal maintenance investment, and repurposing older pipelines that may have low utilization for a higher and better use is a crucial skill set of good midstream management teams.

New pipelines are typically constructed to allow shippers or producers to take advantage of significant price differentials (basis differentials) between two market hubs because supply and demand are out of balance. Pipeline operators will enter long-term contracts with shippers to recover the project’s construction and development costs as well as a return on capital in exchange for a reasonable tariff that allows a shipper to capture a profitable differential, and capacity will be added until it is no longer profitable to do so. Regulators approve pipelines only when there is an economic need and pipeline development takes years. The Federal Energy Regulatory Commission and state and local levels provide regulatory oversight, and new pipelines under consideration must contend with demanding environmental and other permitting issues.

A network of pipelines serving multiple end markets and supplied by various regions is typically more valuable than a scattered collection of assets. A pipeline network allows the midstream company to optimize the flow of hydrocarbons across the system and capture geographic differentials, use storage facilities to capture price differentials over time, and direct more hydrocarbons through its system via storage, gathering, and processing assets, ensuring security of flows and higher fees.

Enterprise’s asset base quality is outstanding, ensuring a sustainable competitive advantage for years. For producers seeking options for their hydrocarbons, Enterprise offers an extensive menu. The partnership is connected to every central U.S. shale basin, every ethylene cracker, and 90% of the refineries east of the Rockies and offers export facilities out of the Gulf Coast. The heart of the asset base lies in its comprehensive NGL network, which offers deep access to Mont Belvieu. To further its control over the NGL value chain, Enterprise has built out many petrochemical assets, including propylene pipelines, propane dehydrogenation (PDH), and isobutane dehydrogenation (iBDH) facilities, which allows the partnership to extract higher-value olefins from the feedstock. In effect, the firm is creating more of a demand-pull for the ample supply of NGLs traveling through its network. Enterprise was one of the first companies in the industry to recognize the shortage of NGL infrastructure in the U.S. and the eventual shift toward exports. It has built an impossible-to-replicate collection of assets across the value chain, positioning it to capture differentials between U.S. and international markets.

Enterprise’s natural gas assets are also solid. The network comprises natural gas pipelines across New Mexico, Texas, and Louisiana, with 400-plus interconnection points to demand centers and substantial net gas processing capacity. Most of the network is in Texas. Enterprise has benefited more recently from its exposure to the Permian Basin, where rich gas volumes have more than quadrupled since 2013, and the partnership has added processing capacity to feed its existing asset base.

Enterprise’s crude pipelines are primarily located in Texas, Oklahoma, and New Mexico, connecting the Eagle Ford, Permian, Cushing, and Gulf Coast export hubs. The addition of substantial crude oil export capacity has materially increased the overall value of the asset network. The reversal of the Seaway pipeline to flow oil to the Enterprise hydrocarbon terminal was an intelligent and bold move. The partnership’s position on the Houston Ship Channel is particularly impressive regarding storage and export opportunities. The hydrocarbon terminal can accommodate Suzemax tankers, the largest tankers that can navigate the channel. The company also controls Beaumont West, Freeport, and Texas City systems, which adds dock access. Dock access is essential, given geographic constraints. Replicating Enterprise’s crude oil asset portfolio will be difficult, if not impossible.

Enterprise’s Sea Port Oil Terminal demonstrates the company’s leadership in the industry. This asset has been a work in progress since 2019—we do not currently value its future impact. In late 2022, Enterprise obtained several approvals but has yet to make a final investment decision on this significant oil export effort. If operating, this asset could move up to two million barrels per day of oil and materially change the demand-pull dynamics of oil toward the Gulf Coast if approved. If approved, the Sea Port Oil Terminal could contribute roughly $500 million in annual operating earnings based on an estimated total cost of $3 billion-$4 billion.

Enterprise’s marketing operations are an essential asset that allows the company to collect significant additional fees from its network versus being a pure toll-taker. With its marketing operations, Enterprise takes ownership of the hydrocarbon. It seeks to exploit differentials based on time, location, or product arbitrage across its system’s hundreds of connection points. This type of asset is challenging to replicate due to the complexity and richness of the company’s system, and the few producers that undertake marketing activities only focus on the relatively few basins they operate in versus the entirety of the U.S. oil and gas complex. It also provides Enterprise full access to profitable opportunities in secondary markets across its pipelines for capacity not being used under firm contracts versus ceding those fees to the shipper.

Other examples include taking advantage of seasonal changes in demand for propane, upgrading opportunities for raw NGLs to be converted to higher grade and more profitable olefins, and using Enterprise’s network to move products to markets where differentials are the widest. Rather than operate as a separate group, the marketing operations are embedded within Enterprise Product’s natural gas, oil, and NGLs teams, providing insights to help them make investments across the portfolio. The marketing operations offer an added benefit in sourcing and developing relationships with producers to serve as committed shippers for future investments. They also serve as sources of internal demand by creating opportunities for the company to take ownership of hydrocarbons and support incremental investments. Peers within the midstream industry without this robust level of marketing operations face higher hurdles in obtaining commitments for significant investments.

Pipeline contracts provide durable returns on invested capital. Initial contracts by shippers to reserve capacity on Enterprise’s new pipelines are typically fifteen to twenty years. These industry-standard contracts provide shippers with reserved capacity, for which they pay an origination fee. However, they do not obligate them to use the line if better opportunities exist elsewhere, for which the shipper would pay an additional transport fee. For Enterprise’s latest investments, at the PDH plant, 100% of the 750,000 pounds per day are contracted for fifteen years, and the iBDH plant is also fully contracted for fifteen years, split between investment-grade companies and internal Enterprise marketing capacity. In times of market stress, Enterprise has also been creative with its assets, obtaining area dedication contracts where the producers would be obligated to provide a certain number of barrels per day and then looking to convert the contract to a long-term fee contract as the markets recover. This effort facilitates the long-term development of relationships with essential producers.

Enterprise Products Partners has consistently been a thoughtful allocator of capital toward midstream projects, seeking to protect the balance sheet through the cycle and maintaining a reasonable stance on capital allocation for unitholders. Enterprise retains sufficient distributable cash flow to reinvest in the business while limiting reliance on dilutive equity and debt capital market issuances. One should note the Oiltanking acquisition in 2015 for a total consideration of $6 billion as a forward-thinking effort to capture growing export opportunities.

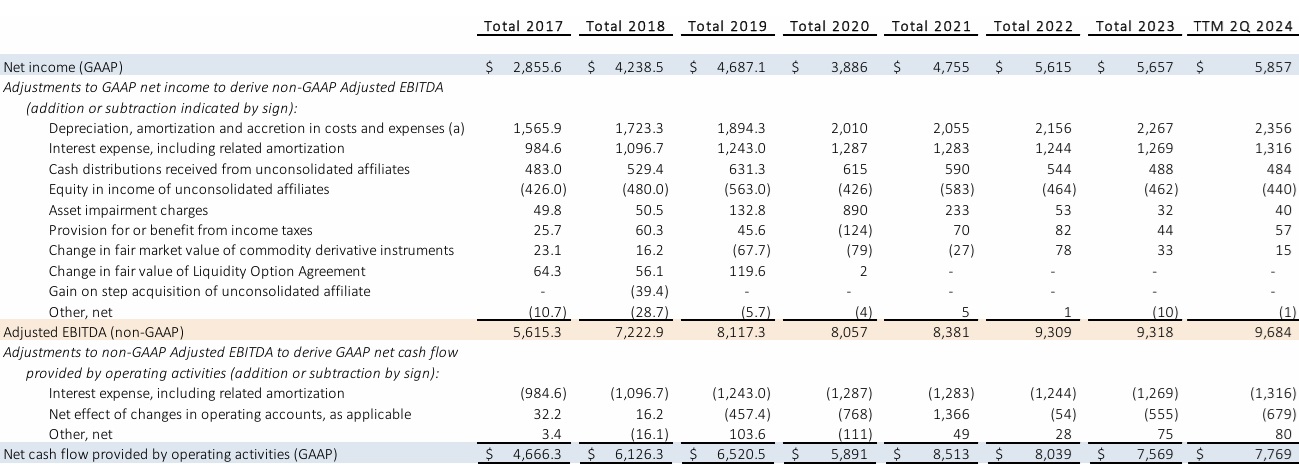

Management has pursued a prudent approach to achieving consistent, steady growth and returns. The achievement of self-funding the equity portion of its capital expenditure program a year ahead of schedule, plus the announcement of a $2 billion unit buyback, further reinforces our conviction in the company’s management team. Enterprise has used almost half of its $2 billion unit-buyback program. Enterprise bought back $186 million in units in 2020, $214 million in 2021, $250 million in 2022, and $187 million in 2023. The Navitas deal for $3.25 billion in early 2022 consumed most of the company’s excess capital. Still, the near-term upside from the deal is likely already above expectations in the current market. As an equity participant, we are pleased with the results.

As capital spending fluctuates with the industry’s cyclical nature, Enterprise has ensured the balance sheet remains healthy. Leverage ratios are kept at prudent levels, and maturities are managed appropriately. The partnership has also recognized the more limited value investors place on the unit distribution and slowed growth to appropriate levels, freeing up capital to be invested elsewhere at better returns. Enterprise also emphasizes excess cash flows after distributions and capital spending, another welcome and investor-friendly development that sends a meaningful signal to the rest of the industry.

Enterprise’s exemplary stewardship of its business mitigates concerns about the limited rights of limited partner unitholders. The current governance structure affords LP unitholders almost no say in the firm’s management. However, management’s consistent alignment with LP unitholders’ interests over time substantially differentiates it from midstream peers. The continued participation (and reinvestment of approximately $100 million annually) from the Duncan family (the partnership’s original co-founder and general partner) in the LP is a powerful endorsement of the founding family’s long-term investment commitment.

Valuation

Profitability within the gas gathering and processing business and incremental marketing contributions drive the company’s intrinsic value. Our fair value estimate of $38 per unit implies a 2026 multiple of fifteen times free cash flow and a distribution yield of 7%. Enterprise’s main driver will be its natural gas liquids segment, as the demand from international markets for various industrial applications lets it take advantage of export opportunities and lucrative differentials via its comprehensive asset base.

The petrochemicals segment should continue to do well. Completing the PDH 2 plant in 2023 will be a significant addition for 2024 and beyond. Increased demand for ethane and ethylene will benefit Enterprise Products. The company’s asset base’s diversity, ability to take advantage of any profitable opportunity in the U.S. midstream, and its largely fee-based earnings stream all support growth opportunities. Still, U.S. volume growth will likely be slower over the next few years as U.S. hydrocarbon producers primarily operate within operating cash flows. As a result, we expect operating profits to increase by about 3% annually in the latter stages of our forecast. New projects entering service are offset by weaker processing margins due to lower oil and gas prices and utilization over time from a record 2022 for gas processing.

Enterprise’s Sea Port Oil Terminal has been a work in progress since 2019 and is not included in our valuation model. Enterprise obtained several approvals but has yet to make a final investment decision on this significant oil export effort. If approved, we would expect it could move up to two million barrels per day of oil and materially change the demand-pull dynamics of oil toward the Gulf Coast. We estimate it could contribute about $250-$500 million to annual operating profits based on an estimated total cost of $2 billion-$4 billion. Enterprise has suggested construction costs below $3 billion, indicating the lower end of estimates is likely.

Investments Risks

As the most significant player in the NGL market, Enterprise is most leveraged to meet petrochemical demand in the Gulf Coast and international markets. Its expansion into petrochemical activities insulates Enterprise from midstream cyclicality. Enterprise’s marketing activities let it extract additional fees from its asset base while providing insights into each market. The marketing operations depend on differential spreads that could continue to narrow without investments by Enterprise and third parties to spur demand. If the promise of a significant increase in NGL demand from China and India never materializes, Enterprise Products Partners is left with capital sunk in export facilities. Without substantial growth in U.S. hydrocarbons, more of Enterprise’s assets risk being underutilized and thus seeing lower revenue and fees.

Enterprise’s primary risk is declining demand for natural gas liquids, as its NGL business constitutes over 50% of the partnership’s gross operating margin. However, its petrochemicals business looks to be the most critical earnings driver in the near to medium term. Therefore, delays or reduced demand from international markets, such as critical petrochemicals markets like India or China, would negatively affect Enterprise’s earnings. Even as much of the downside risk is mitigated by sufficiently contracted capacity, failure of NGL or petrochemical demand to materialize would limit Enterprise’s earnings upside.

Enterprise is also exposed to several significant environmental, social, and governance risks, including an eventual peak and decline in U.S. oil demand and managing its carbon emissions and potential costs. Its petrochemicals business offers growth opportunities but also introduces additional health and safety concerns and new potential chemicals-related legal liabilities. Risks include environmental damage from chemical waste around a manufacturing site. This typically results in remediation and litigation expenses ranging from tens of millions to over one billion dollars, depending on the extent of the damage.

As with many yield-oriented investments, Enterprise units could underperform if interest rates increase faster than expected. A steepening yield curve increases the predicted yield for competing assets.

Material ESG exposures create additional risk for midstream investors. In this industry, the most significant exposures are greenhouse gas emissions (from upstream extraction, midstream operations, and downstream consumption) and other emissions, effluents, pipeline spills, and opposition and protests. In addition to the reputational threat, these issues could significantly force climate-conscious consumers away from fossil fuels, resulting in long-term demand erosion. Climate concerns could also trigger regulatory interventions, such as production limits, removal of existing infrastructure, and perhaps even direct taxes on carbon emissions.